Back taxes don’t go away on their own. The balance grows every month – penalties on top of interest, interest on top of the original debt – and the IRS has collection tools that most people don’t think about until one of them hits. Wage garnishments. Bank levies. Federal liens that attach to property and surface when you try to sell or refinance. If you owe and haven’t done anything about it, the gap between where you are and where you need to be gets wider every month you wait.

The IRS has a few programs for people who can’t pay their tax bill in one lump sum. If you aren’t sure which one is right for you, you’re in the right place.

Key Takeaways

- File your return even if you can’t pay – the failure-to-file penalty runs 5% per month (up to 25%), which is ten times the failure-to-pay penalty of 0.5% per month

- Short-term IRS payment plans give you 180 days with no setup fee

- An approved installment agreement cuts your monthly penalty rate from 0.5% to 0.25% and stops most collection actions

- An Offer in Compromise can settle your balance for less than you owe – the IRS accepts roughly 40-45% of submitted offers

- If you’ve filed on time for the past three years with no penalties, First-Time Abatement can wipe out penalties entirely

- Balances certified as seriously delinquent (currently $62,000) can trigger passport revocation

What the IRS Actually Does When Back Taxes Go Unresolved

Most people expect a bill. What they get instead is a process that escalates in stages, and each stage gives you fewer options than the one before it.

If you owe taxes and never filed a return, the IRS prepares one for you. They call it a Substitute for Return (SFR). It doesn’t use your deductions. It calculates tax using only the income documents they have on file – W-2s, 1099s – and it will almost always be higher than what you’d owe if you filed yourself. I’ve had clients come in with SFR assessments of $40,000 or more who, after we filed their actual return, ended up owing under $10,000. That gap is common, and it matters, because the IRS pursues the SFR number until you replace it.

Once a balance is assessed, the IRS can file a Notice of Federal Tax Lien. A lien attaches to everything you own – real estate, vehicles, financial accounts. It’s public record. It affects your credit, complicates any property sale, and tells every other creditor that the IRS gets paid first.

After the lien comes the levy. That’s the actual taking. The IRS can drain a bank account, pull wages directly from your paycheck, and in more serious situations, seize real property or even your vehicle. Understanding exactly when the IRS can take your car, and what protects you is worth knowing before collection reaches that stage. They are required to send a Final Notice of Intent to Levy before doing it – but that notice goes to the last address they have on file, and if you’ve been ignoring prior letters, it may arrive looking like just another envelope.

One thing most people don’t expect. If the IRS certifies your balance as seriously delinquent – currently set at $62,000, adjusted for inflation annually – they notify the State Department. Your passport can be revoked or denied until the debt is resolved. That catches people off guard, especially when it comes up during travel plans.

Check the Number Before You Do Anything Else

Don’t accept the IRS’s balance as accurate without checking it yourself. They make errors. SFR filings are wrong by design – not fraudulently, but structurally, because they don’t have your full picture. Even manually assessed balances sometimes include duplicate entries, misapplied payments, or penalties that should have been abated. Challenging IRS errors before agreeing to pay is always worth the time.

Pull your transcripts first. Go to IRS.gov and request your Account Transcript – that shows the assessed balance and every action on your account. Then get your Wage and Income Transcript, which shows every document third parties reported about you. If the income on the IRS’s SFR doesn’t match what you actually earned, that’s worth addressing before you agree to pay anything. Call 800-908-9946 if you’d rather do it by phone.

If you received a Notice of Deficiency, you have 90 days to either file a petition in Tax Court or file an original return. That’s a hard deadline. After it passes, the assessed amount is locked in and you lose the right to contest it in court. Most people don’t realize that window exists, which is part of why SFR balances stick.

File the Return First – Even If You Can’t Pay

This is where a lot of people make a costly mistake. They don’t file because they can’t pay, thinking the filing itself triggers the problem. It doesn’t. Not filing makes it worse.

The failure-to-file penalty is 5% of unpaid taxes per month, capped at 25% of the total balance. The failure-to-pay penalty is 0.5% per month, also capped at 25%. File without paying and you’re facing only the smaller one. Skip filing entirely and both penalties run simultaneously – and the filing penalty is ten times the payment penalty. The math on waiting makes no sense in your favor.

Filing also replaces any SFR the IRS may have prepared. Whatever inflated number they computed on your behalf gets wiped out by your actual return. If you have deductions that reduce your balance by $15,000 or $20,000, the only way to get credit for them is to file. Our attorneys handle multiple years of unfiled returns regularly – it’s a more common starting point than most people realize.

Late returns are accepted with no cutoff. The IRS takes returns going back many years. There is no statute of limitations on filing a return that was never submitted – only on collecting after one has been assessed.

IRS Payment Options When You Can’t Pay in Full

Once you’ve filed, or if you already have an assessed balance, you have real choices. Which one fits depends on your balance, your income, what you own, and how long this has been building.

Short-Term Payment Plan

If the full balance is within reach in the next six months, the IRS short-term plan is worth knowing about. No setup fee. You get 180 days to pay. The 0.5% monthly penalty and current interest (7% annually, though that rate adjusts quarterly) keep running, so paying sooner saves money – but there’s no formal application, no financial disclosure, and you apply through the IRS Online Payment Agreement tool in a few minutes.

This option is underused. A lot of people jump straight to a long-term installment agreement when they’re actually close enough to the end of the debt that 180 days would cover it. If you’re expecting a bonus, a tax refund, or a property closing in the next several months, run the 180-day math before assuming you need a multi-year plan.

Long-Term Installment Agreement

For balances you genuinely can’t clear in six months, a long-term installment agreement gives you up to 72 months. Setup fees run $22 for a direct debit plan through the Online Payment Agreement tool, or $69 for a non-automatic payment plan. Low-income taxpayers may qualify for a fee waiver.

The less-known part of how installment agreements work. Once the IRS approves your plan, your monthly failure-to-pay penalty rate drops from 0.5% to 0.25%. That’s not huge, but on a $30,000 balance over four years, it adds up. The collection clock also pauses – while an agreement is pending or active, the IRS is prohibited from issuing a levy. That’s the actual reason to get into a plan quickly, not just to make monthly payments more manageable.

Balances under $50,000 can be set up online with Form 9465 – no financial disclosure required. Above $50,000, the IRS requires Form 433-A or 433-F, which documents your full financial picture. How you present that form matters more than most people realize. Our attorneys work through this regularly and know what the IRS is actually looking for when they review it.

Currently Not Collectible Status

If you genuinely cannot pay anything right now without falling behind on housing, food, utilities, or medical care, you can request that the IRS temporarily suspend collection activity. This status is called Currently Not Collectible, and it does exactly what it sounds like – the IRS pauses active collection while you’re in it.

To be clear about what CNC does and doesn’t do. It stops levies and garnishments. It does not stop interest from accruing. The debt doesn’t shrink. The IRS will review your status periodically and resume collection when your finances improve. Think of it as buying time, not as a resolution. For someone who just lost a job or is dealing with a medical situation, buying time is sometimes exactly what’s needed – just go in knowing what you’re getting.

Offer in Compromise

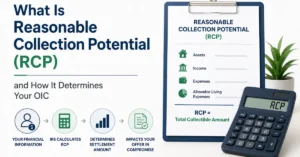

An Offer in Compromise (OIC) settles a tax debt for less than the full amount owed. The IRS accepts them when the offered amount equals or exceeds what they calculate they could realistically collect from you – your income, your assets, and your expenses factored together into a number they call your Reasonable Collection Potential (RCP).

If your RCP works out to $12,000 and you owe $75,000, the IRS may accept $12,000 as full payment. That’s the real value of an OIC – not that it’s a negotiation in the traditional sense, but that the IRS has a formula, and if you fit the formula, they take it.

OICs can be paid as a lump sum in five or fewer installments over five months, or in periodic payments spread over 24 months. Lump sum offers require a 20% non-refundable deposit with the application. Acceptance rates run roughly 40-45% of submitted offers – which sounds reasonable until you look at why the rejected ones fail. Most are rejected because the RCP was calculated wrong, not because the person didn’t qualify. The IRS recalculates it themselves when they review your offer. If the numbers don’t align, you get a rejection and start over. Our attorneys build these with that in mind.

Penalty Abatement – Reducing What You Actually Owe

Penalties can easily represent 25% or more of a back tax balance. In some cases they’re removable, and that’s worth pursuing before agreeing to pay a balance that includes them.

First-Time Penalty Abatement

First-Time Abatement (FTA) is a one-time IRS administrative waiver that removes failure-to-file, failure-to-pay, or failure-to-deposit penalties – no explanation required. The only condition is a clean three-year compliance history. You filed on time, paid on time, and didn’t receive penalties in the three years before the year you’re requesting relief for.

You call the number on your IRS notice, ask for penalty relief under First-Time Abatement, and if you qualify, the IRS processes it over the phone. Most people don’t ask. That’s not me saying the IRS is hiding it – it’s just not something they lead with. If you’ve already paid penalties that you could have had removed, file Form 843 and request a refund. The IRS will review it.

One real limitation to flag. FTA removes penalties up to the date you request it. If you still have an unpaid balance after the abatement, the failure-to-pay penalty starts accruing again from that point forward. Getting penalties removed without resolving the underlying balance just restarts the clock. It should be paired with a payment plan or full payment, not treated as a standalone fix.

Reasonable Cause Relief

If FTA doesn’t apply, penalties can still be removed by demonstrating reasonable cause – a legitimate reason outside your control. Serious illness, hospitalization, a natural disaster, or death of an immediate family member are examples the IRS accepts. What they don’t accept is not knowing you had to file, an advisor who made an error on your behalf, or simply not having the money. The IRS’s position is that lack of funds means you should have borrowed, sold assets, or made partial payments. Harsh, but that’s the written standard.

Reasonable cause requests require documentation – not just a letter explaining what happened. Medical records, insurance claims, disaster declarations, legal records. Anything that corroborates the timeline. A well-documented request gets reviewed on its merits. An undocumented request almost always gets denied regardless of how valid the underlying reason is.

Bankruptcy and Tax Debt – What Actually Qualifies

Bankruptcy can discharge tax debt, but the conditions are specific enough that most people who think they qualify don’t. The IRS collection process has more built-in flexibility than bankruptcy in most cases, which is why it should be the last option you look at, not the first.

Under Chapter 7, income tax debt may be dischargeable if five conditions are all met. The debt must be from income taxes only (not payroll taxes, not fraud penalties). The return was due at least three years before the bankruptcy filing. The return was actually filed at least two years before filing. The tax was assessed at least 240 days before filing. And there was no fraud or willful evasion. All five conditions, for each tax year in question. One missed condition for one year means that year’s debt survives.

Payroll taxes – the employer portion of Social Security and Medicare – almost never qualify for discharge. Tax fraud penalties never do. The automatic stay that bankruptcy triggers only pauses IRS collection temporarily for debts that won’t ultimately be discharged anyway.

The longer-term issue with bankruptcy is the credit impact and the collateral damage to any business relationships, financing, or professional licenses that require financial standing. Before filing, it’s worth having an attorney compare the discharge outcome against what you’d get from an Offer in Compromise or installment agreement. In a lot of situations, the OIC leaves you in a better position without the bankruptcy on record.

Frequently Asked Questions About Back Taxes

How far back can the IRS collect?

Ten years from the date the tax is formally assessed. That window is called the Collection Statute Expiration Date (CSED). Several actions pause it – filing bankruptcy, submitting an OIC, requesting a Collection Due Process hearing, or spending extended time outside the United States. If you’re banking on the 10-year clock expiring, any of those events add time back onto it. Counting on statute expiration as a strategy tends to go wrong.

Do I need a tax attorney or can I handle this myself?

For a simple installment agreement on a balance under $50,000, or a first-time abatement request with a clean compliance history, you likely don’t need professional help. For anything involving an OIC, multiple unfiled years, a Substitute for Return you need to replace, or collection actions that have already started, an attorney changes the outcome – specifically because of attorney-client privilege. Communications with a tax attorney are protected. That protection doesn’t apply to your CPA, and it matters when the case involves anything the IRS might later treat as criminal.

What if I literally can’t pay anything monthly?

Request Currently Not Collectible status. You’ll submit a financial statement showing your income doesn’t cover basic living expenses, and if the IRS agrees, collection pauses. You need documentation – pay stubs, bank statements, monthly bills – that supports what you’re claiming. The IRS audits CNC requests, and unsubstantiated claims get denied. If your situation changes, they’ll reassess. But while you’re in that status, bank levies and wage garnishments stop.

Does resolving back taxes help my credit?

A federal tax lien is public record and affects your credit profile even though the major bureaus removed most tax lien data from consumer reports in 2017-2018. The lien still appears in public record searches that lenders run outside the standard credit pull. Once you’ve resolved the balance, you can request lien withdrawal using Form 12277. That removes it from the public record entirely – not just marks it as satisfied. Withdrawal is different from release: release means the debt is paid, but the lien history remains. Withdrawal removes the record.

How long does an OIC review take?

The IRS has 24 months from submission to accept or reject. In practice, most offers resolve in 6 to 12 months. Collection is generally suspended during the review period. If the IRS hasn’t acted by the 24-month mark, the offer is automatically accepted by law – though that outcome is rare and usually results from administrative backlog.

What to Do Now

The single worst move with back taxes is inaction. Every month the balance sits unaddressed, interest accrues, penalties may accrue, and the IRS gets closer to a collection action that forces your hand.

Pull your Account Transcript at IRS.gov and confirm the actual assessed balance. File any unfiled returns before anything else – even without payment. Once you have the real number, evaluate whether a short-term plan, an installment agreement, Currently Not Collectible status, or an Offer in Compromise fits where you are.

Silver Tax Group handles IRS back tax cases every week. We stop active collection, get installment agreements approved, and build Offers in Compromise. If you’ve received notices and haven’t responded, or collection activity has started, call us today for a free consultation.