Ever found yourself staring down the barrel of a form 433-f, with the IRS on one end and your hard-earned money on the other? That’s what it can feel like when you’re up against tax debts, wrestling through piles of paperwork. Seems like a daunting task, pitting yourself against an opponent far greater than you.

The complex language…the unending sections… can be downright intimidating. But here’s some good news: just because it feels like David vs Goliath doesn’t mean there isn’t hope.

This post is your slingshot – providing practical guidance to help navigate Form 433-F, IRS payment plans, installment agreements, and more. Stick around for valuable tips about accurately completing this form without breaking a sweat or missing any crucial details.

Understanding Form 433-F and Its Purpose

The IRS Form 433-F, also known as the

Collection Information Statement, plays a pivotal role in IRS collections. If you’re swimming in tax debt or have been contacted by IRS revenue officers, this form is your lifeline.

This form collects financial information from individuals with taxes owed – kind of like a detective collecting clues to solve a mystery. It’s used to determine eligibility for payment plans and uncollectible status – the Sherlock Holmes of forms if you will.

Key Stats:

- The average American might find dealing with the IRS daunting but remember, knowledge is power.

- Around 14 million Americans end up owing taxes each year.

- In fact, it’s estimated that taxpayers owe nearly $131 billion in back taxes (including penalties).

If you are one among those millions, don’t worry. The Silver Tax Group has got your back. Our experienced team understands every line and box on this form better than they understand their own family trees – after all; we deal with it daily.

Determining Eligibility: A Detective Story With Numbers

You see, completing Form 433-F feels more like an intense game of Sudoku rather than just filling out another mundane document because there’s quite some math involved here. From analyzing non-wage household income to calculating monthly living expenses – everything counts when determining whether someone qualifies for help from Uncle Sam regarding their outstanding balance.

Navigating Through Payment Plans & Uncollectible Status

We know that juggling real estate list values while accounting for personal care costs can feel overwhelming – akin to spinning plates while balancing on a tightrope. But getting these details right is crucial. They help the IRS consider if you are eligible for an installment agreement request or whether your debt can be marked as uncollectible.

Think of Form 433-F as a crystal ball. Form 433-F provides the IRS with a glimpse into one’s fiscal situation, aiding them in determining the most effective means to resolve any unpaid taxes.

Key Takeaway:

Form 433-F reveals your financial future to the IRS, helping them understand whether you need help with your tax debt or not. So don’t worry. With careful attention to each detail and correctly filled out boxes, this form becomes an invaluable tool for navigating through owed taxes.

When to Use Form 433-F

If you’re up against a tax debt, knowing when and how to use IRS Form 433-F is key. This form helps the IRS assess your financial situation, determining eligibility for payment plans or uncollectible status.

The Right Time for Form 433-F

You might be asking yourself, “Is it time for me to fill out this form?” Well, there are two main scenarios that call for it:

- Your assessed balance exceeds $50,000 and you need a non-streamline payment plan.

- Your proposed monthly payments can’t clear your tax liability within six years (72 months).

This makes sense because the IRS wants more information before setting up a long-term payment plan or writing off substantial amounts of money as uncollectible.

More Than Just Tax Debt?

Sometimes though life throws us curveballs – maybe an unexpected medical bill lands in your lap or you lose your job. In such cases where paying off taxes could lead to serious hardship – don’t panic. You can still submit Form 433-F with documentation supporting these hardships. This isn’t just about being unable to pay; it’s also about maintaining dignity while facing financial difficulties.

Navigating Other Complexities

In some situations, other factors come into play too. If direct debit doesn’t work well with how you manage finances and if what you owe lies between $25k-$50k – yep, again we’ll need this magic little form called Form 433-F.

In the past, this form was mandatory for tax liabilities over $50k. However, now it’s requested only by revenue officers or when you need to show hardship.

When Revenue Officers Ask For It

The IRS is always on the hunt for vital information. Don’t take it lightly when they ask for Form 433-F during an audit or collection process. Cooperate.

Completing Form 433-F Accurately

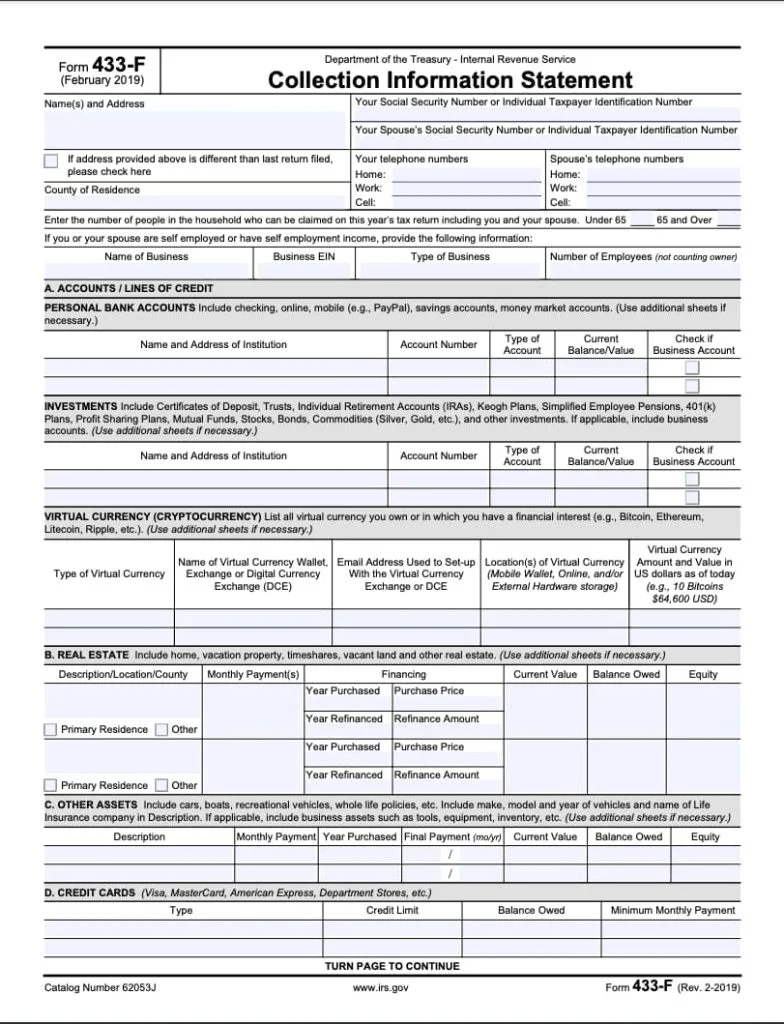

Filling out Form 433-F accurately is a critical step in managing your tax debt. The form consists of different sections covering personal information, accounts, real estate, assets, credit cards, business information, employment information, household income, and monthly living expenses. Each section requires careful attention to ensure accurate reporting.

Personal Information and Contact Details

The first section of the form requires you to fill out your personal information and contact details. This includes your name, social security number or employer identification number, and mailing address. Take the time to make sure that your personal information and contact details, such as name, social security number or employer identification number, and mailing address are accurate.

If you are a business owner seeking assistance with delinquent taxes tied to an Employer Identification Number (EIN), use the EIN instead of your Social Security Number in this section.

Household Income and Expenses

In this section, you need to report all sources of income, including wages from employment or self-employment income if applicable. Additionally, you should report any non-wage household income, such as rental income or social security payments. In this section, you must accurately report your monthly expenses such as housing costs and out-of-pocket medical expenses in order to determine if you qualify for uncollectible status due to hardship cases. This information will be assessed by IRS revenue officers to determine if you qualify for uncollectible status due to hardship cases involving substantial life changes that have negatively impacted your finances.

Assets and Liabilities

In this section, you need to provide details about all your financial assets, including bank accounts, mutual funds, life insurance policies with cash value, and retirement plans. Additionally, you should include information about your physical properties, including your primary residence and any vacation homes. It is essential to remember that when cataloging commercial holdings, it should not only be significant acquisitions like real estate but also minor assets such as accounts receivable and available credit on corporate charge cards. These assets contribute to the total asset value, which can significantly impact the outcome of your installment agreement request.

Finally, remember to list all your debts. This includes credit card balances and any loans you’re paying off.

Key Takeaway:

Filling out Form 433-F is crucial for managing tax debt. You need to carefully provide personal details, income sources, living expenses, and information about assets and liabilities. Accuracy in reporting these can affect your eligibility for hardship cases or installment agreements. So take your time to get it right.

Payment Plans & Installment Agreements via Form 433-F

Dealing with tax debt can be a daunting task, but the IRS provides resources to help you manage your balance owed. The IRS offers options like payment plans and installment agreements to help you manage your balance owed. These are great ways for taxpayers who owe money to the IRS but cannot afford to pay all at once.

The form used in this process is called Form 433-F (Collection Information Statement). This document collects financial information about you and helps the IRS determine eligibility for these programs based on your household income, living expenses, real estate owned, credit card balances, and bank accounts among other factors.

If you’re looking at delinquent taxes or struggling with monthly living expenses because of tax obligations piling up – don’t panic. Completing Form 433-F may seem daunting; however, working with a licensed tax professional when filling out this paperwork can ease some of that stress. They will ensure that all necessary details such as social security number and mailing address are correctly filled out avoiding common mistakes which could delay processing time or even worse – result in rejection.

Navigating Payment Plans

A typical solution offered by the IRS after reviewing your completed form is setting up an installment agreement request where they allow making payments over time until the final payment clears off any outstanding debts owed by clients. But remember not everyone qualifies immediately upon submission of their forms so always keep copies handy should there need further review later down the line.

Finding Relief Through Installment Agreements

An alternative path often taken if approved from submitting Form-433F involves being placed under a status known as “currently uncollectible”. This means essentially pausing collection efforts due amount falling below certain thresholds set forth by the IRS itself – providing temporary relief until the situation improves financially speaking.

However, bear in mind that you must continue to file future tax returns and pay anything owed for these years even if your previous debt is under uncollectible status or part of an installment agreement. Not doing so can lead to a default on the agreement and an immediate full payment requirement.

Navigating Complexities & Exceptions with Form 433-F

Let’s face it, tax forms can be tricky. Navigating Form 433-F can be a daunting task, with many complexities and exceptions to consider. But don’t worry. I’m here to help you traverse this labyrinthine path.

Uncollectible Status and Hardship Cases

Form 433-F is a beast of its own kind, especially when dealing with uncollectible status or demonstrating financial hardship. In fact, in the past, Silver Tax Group’s clients had to submit this form for tax liabilities over $50k. But now? It’s only required if requested by an IRS revenue officer or for hardship cases.

This change has brought relief but also confusion among taxpayers because not everyone fits neatly into these categories. So how do we determine eligibility?

The key lies in providing accurate information about your finances – from bank accounts and credit cards to real estate assets and monthly living expenses – everything matters.

You might ask, why do they need all these details? The answer is simple: The more detailed your financial snapshot is; the better equipped the IRS will be in determining whether you qualify for payment plans or uncollectible status.

A good rule of thumb? Be honest and comprehensive while completing this form – remember any attempt at hiding assets could backfire badly.

Credit Cards vs Living Expenses:

| Credit Cards | Living Expenses | |

|---|---|---|

| Ideal Situation | No Outstanding Balance | Within IRS Standards |

| Risk Factor | High Outstanding Balance | Beyond IRS Standards |

You might be wondering what this table means. It’s pretty straightforward. If you have no outstanding balance on your credit cards and your living expenses are within the IRS standards, that’s an ideal situation.

Working with IRS Revenue Officers & Professional Assistance

If you’re dealing with tax debt, the idea of working directly with IRS revenue officers can be intimidating. But don’t let that fear lead to procrastination or inaction.

IRS revenue officers are trained professionals whose job is to collect taxes owed and secure delinquent tax returns. They’ll review your financial statement (think Form 433-F) and assess your ability to pay.

The Form 9465, or Installment Agreement Request, should accompany a completed Form 433-F when sent off to the IRS along with a copy of your tax return. This process can help facilitate payment plans for clients who owe back taxes.

Navigating Negotiations

A crucial part of this journey involves negotiation – which is where professional assistance comes into play.

Hiring an experienced licensed tax professional will give you peace of mind because they have dealt with similar cases before. Their expertise helps ensure accuracy when completing forms like the complex Form 433-F.

Safeguarding Your Interests

Involving professionals, like the experts at Silver Tax Group, doesn’t just mean more accurate paperwork—it also means having someone on your side who knows how these processes work and what rights you have as a taxpayer.

This guidance could be beneficial if in a “not collectible” status—a temporary hold on collections due to hardship—is something you need help navigating through.

Let The Tax Experts Take Over

By leaning on the expertise of a tax attorney, you can navigate the complex tax landscape with confidence. This not only helps alleviate your stress but also protects your interests when dealing with IRS officials.

Key Takeaway:

Don’t let tax debt intimidate you. IRS officers are there to help, not hinder, by reviewing your Form 433-F and setting up payment plans if needed. Hiring a tax attorney can certainly ease the process, ensuring accuracy on complex forms like Form 433-F and protecting your interests during negotiations.

Avoiding Common Mistakes with Form 433-F

Filling out Form 433-F can be tricky, especially when it comes to details like social security numbers and mailing addresses. But a simple mistake could cause your form to get rejected or lead you into deeper tax debt.

Getting Personal Information Right

The first section of Form 433-F requires your personal information such as name, address, and most importantly – Social Security Number (SSN). Make sure this data is accurate because mistakes here can result in delays or worse – misidentification issues.

Business owners also need their Employer Identification Number (EIN) ready. It’s surprising how often these crucial identification numbers are either wrong or missing entirely on submitted forms.

Detailed Financial Statement: Income & Expenses

Your financial statement includes both wage and non-wage household income sources like rental income or social security payments which must be clearly detailed on the form. Any confusion between monthly living expenses and total living expenses could put you at risk for an audit if not corrected before submission.

You might think that underreporting certain incomes would help reduce your perceived ability to pay but remember IRS officers have seen it all. They’re experts in sniffing out inconsistencies which may just make them dig deeper into your finances.

Careful Reporting of Assets & Liabilities

In addition to real estate holdings including primary residence and vacation homes, bank accounts too fall under assets that should be listed accurately along with their current balances. Even life insurance policies count towards asset calculation so don’t leave those off either.

Sometimes people forget about other liabilities they hold outside credit cards such as mutual funds, stocks, and accounts receivables. IRS considers all of these when determining your payment plan or if you qualify for the uncollectible status.

Submitting Form 433-F

Finally, after you’ve thoroughly checked all other details on the form, make sure to sign it. Surprisingly enough, many people often forget this crucial step.

Key Takeaway:

Form 433-F might be tough, but with a keen eye for details, you can sidestep common errors. It’s crucial to get your personal info right and remember key identification numbers like SSN or EIN. Be sure to list all income sources and expenses clearly to minimize audit risks while reporting assets and liabilities accurately. Finally, make sure not to overlook the vital step of signing the form.

Common Questions & Answers Around Form 433-F

What level of detail is required for my financial information on Form 433-F?

When completing Form 433-F, clarity and precision are key. This means providing detailed information about your income, expenses, assets, and liabilities. It’s not just about stating your monthly income; it’s about breaking down all sources of income, regular expenses, and even occasional expenditures. Our experienced tax attorneys can help you compile and present this information effectively, ensuring nothing important is overlooked.

Can IRS Form 433-F affect my offer in compromise (OIC) application?

Absolutely. Think of Form 433-F as the foundation of your OIC application, much like the roots are to a tree. It supports and justifies your offer to the IRS. A well-prepared Form 433-F can be the difference between acceptance and rejection of your OIC. Our tax attorneys specialize in crafting strong OIC applications, using the form to strengthen your case for a favorable resolution.

What if I make a mistake on IRS Form 433-F?

Mistakes on Form 433-F can be like wrong turns on a road trip – they can lead you off course and delay your journey to tax resolution. Inaccuracies might result in unfavorable payment plans or even trigger audits. This is where our tax attorneys come in. We meticulously review your form, ensuring accuracy and completeness to keep your journey toward tax resolution on track.

Is updating the information on Form 433-F a one-time task?

Not quite. Your financial situation is dynamic, like the ebb and flow of the tide. The IRS understands this, and so might request updated information if there are significant changes in your income, expenses, or assets. Keeping Form 433-F current is crucial, especially when you’re on a payment plan or have an ongoing OIC. Our tax attorneys can help you maintain an up-to-date and accurate representation of your financial situation, ensuring smooth interactions with the IRS.

Why should I consider professional assistance for Form 433-F?

Navigating the complexities of IRS Form 433-F can be akin to sailing in uncharted waters. Our tax attorneys are seasoned navigators, adept at charting the best course for your unique situation. We provide expert guidance, from gathering the necessary information to advocating on your behalf with the IRS. Our aim is to secure the most favorable outcome for you, leveraging our knowledge and experience to ease your tax burden.

Squash Your Tax Debt with Help From Silver Tax Group

Cracking the code of Form 433-F is no longer a riddle. You now know its purpose, when to use it, and how to fill it accurately.

You’ve learned about payment plans and installment agreements – tools that can help manage your tax debt. Plus, you’re aware of potential complexities and exceptions that may come up along the way.

Navigating IRS paperwork doesn’t have to be a David vs Goliath battle anymore. With this guide in hand, tackling Form 433-F becomes less daunting.

In closing remember: never shy away from seeking professional assistance if needed. Your hard-earned money deserves smart handling! Contact the experts at Silver Tax Group today!