The IRS Fresh Start program isn’t a single application you file. It’s a collection of tax relief options the IRS made more accessible starting in 2011 to help taxpayers resolve back taxes.

If you owe $50,000 or less, are current on tax filings, and can demonstrate financial hardship, you may qualify for installment agreements, offers in compromise, penalty relief, or currently not collectible status. These are real IRS programs with specific eligibility requirements and formal application processes.

I’ve spent more than 15 years helping clients navigate IRS collection alternatives. I’ve seen taxpayers settle six-figure tax debts for a fraction of what they owed through properly structured offers in compromise. I’ve also seen taxpayers waste months pursuing options they don’t qualify for because they didn’t understand the requirements.

The Fresh Start program expanded access to existing relief options by raising dollar thresholds, reducing documentation requirements for certain payment plans, and changing when the IRS files tax liens. But “Fresh Start” is a marketing term the IRS used to describe these changes – not a separate program you apply for.

What matters is understanding which specific relief option fits your situation, whether you meet the eligibility requirements, and how to structure your application to maximize approval chances.

The IRS receives approximately 49,000 offers in compromise annually but accepts only about 30-36%. Installment agreements have much higher approval rates but don’t reduce what you owe. Currently not collectible status provides temporary relief but interest continues accruing.

Choosing the wrong option – or applying before you qualify – costs you time, money, and creates additional IRS scrutiny.

What the IRS Fresh Start Initiative Actually Includes

The Fresh Start initiative implemented in 2011 and expanded in subsequent years made several key changes to how the IRS handles tax debt collection.

Increased Tax Lien Thresholds

Previously, the IRS filed federal tax liens for relatively small unpaid tax balances. Under Fresh Start, the IRS generally won’t file a tax lien unless you owe more than $10,000 (increased from $5,000).

Tax liens are public records that severely damage credit scores and prevent property sales or refinancing. Raising the threshold means fewer taxpayers face this severe collection action.

If the IRS already filed a lien, you may qualify for lien withdrawal after entering a direct debit installment agreement and making three consecutive payments (for debts under $25,000).

Streamlined Installment Agreements

Fresh Start increased the threshold for streamlined installment agreements from $25,000 to $50,000. If you owe $50,000 or less, you can qualify for a payment plan of up to 72 months with minimal financial documentation.

Small businesses owing $25,000 or less can obtain streamlined agreements for up to 24 months.

These streamlined agreements require less financial disclosure and faster approval than traditional installment agreements requiring detailed Form 433-A or 433-B financial statements.

Expanded Offer in Compromise Eligibility

The IRS modified how it calculates reasonable collection potential for offers in compromise, making more taxpayers eligible to settle for less than full payment.

Changes include allowing more expense categories, reducing the multiplier used for future income calculations, and expanding eligibility for taxpayers earning up to $100,000 annually.

Enhanced Penalty Relief

First-Time Abate penalty relief remains available for taxpayers with clean compliance history. If you haven’t been assessed penalties for the prior three years and meet other requirements, the IRS will abate failure-to-file, failure-to-pay, or failure-to-deposit penalties for one tax year.

Reasonable cause penalty relief continues for taxpayers who can demonstrate circumstances beyond their control prevented compliance (serious illness, natural disaster, death of immediate family member, etc.).

The Four Main Fresh Start Relief Options

Understanding which option fits your situation is critical. Each has different eligibility requirements, approval rates, and consequences.

Installment Agreements: Pay Over Time

Installment agreements allow you to pay your tax debt through monthly payments. This doesn’t reduce what you owe – you pay the full balance plus interest and penalties – but it stops IRS collection actions and gives you time to pay.

Streamlined Installment Agreement:

- Available for balances up to $50,000

- Payment terms up to 72 months

- Minimal financial documentation required

- Can apply online

- Setup fee: $22 for direct debit, higher for other payment methods

Non-Streamlined Installment Agreement:

- Required for balances over $50,000

- Payment terms up to 72 months

- Detailed financial disclosure on Form 433-F or 433-A required

- Monthly payment based on available income after allowed expenses

Eligibility requirements:

- All required tax returns must be filed

- You cannot currently be in bankruptcy

- Current year estimated taxes or withholding must be adequate

- Self-employed taxpayers must be current on quarterly estimated payments

Interest continues accruing during the payment period. The IRS can file a Notice of Federal Tax Lien even after you enter an installment agreement, though direct debit agreements under $25,000 may qualify for lien withdrawal.

If you default on an installment agreement, the IRS can immediately pursue collection through levies and liens.

Offer in Compromise: Settle for Less

An offer in compromise (OIC) allows you to settle your tax debt for less than the full amount owed. This is the option most taxpayers think of when they hear “Fresh Start program.”

But it’s also the most difficult to qualify for and has the lowest acceptance rate – approximately 30-36% of offers are accepted.

The IRS accepts offers in compromise based on three grounds:

Doubt as to collectibility: Your assets and income are less than the full tax liability. This is the most common basis for accepted offers.

Doubt as to liability: A legitimate dispute exists about whether you actually owe the tax. This requires genuine legal or factual questions about the liability.

Effective tax administration: No doubt you owe the tax and could pay it, but requiring full payment would create economic hardship or be unfair due to exceptional circumstances.

Eligibility requirements:

- All required tax returns must be filed

- Current year estimated tax payments must be made

- Business owners with employees must be current on federal tax deposits

- You cannot be in an open bankruptcy proceeding

- You received a bill for at least one tax debt included in the offer

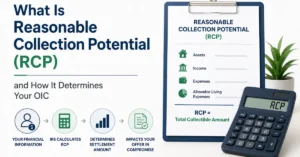

The IRS calculates your reasonable collection potential (RCP) by adding:

- Realizable value of your assets (equity in property, vehicles, retirement accounts, etc.)

- Future income (monthly available income × 12 or 24 months depending on payment terms)

Your offer must equal or exceed your RCP for the IRS to accept it. The IRS uses specific allowable expense standards – you can’t just claim any expense as necessary.

Application process:

- Complete Form 656, Offer in Compromise

- Complete Form 433-A (OIC) for individuals or Form 433-B (OIC) for businesses

- Pay $205 application fee (waived for qualifying low-income taxpayers)

- Pay initial payment (20% for lump sum offers, first payment for periodic payment offers)

- Provide extensive financial documentation

The IRS takes 6-24 months to review offers. During review, collection actions generally pause, but interest and penalties continue accruing.

If your offer is accepted, you must remain compliant with all tax filing and payment obligations for five years. If you fail to file or pay within five years, the IRS can revoke the offer and reinstate the full original debt.

Currently Not Collectible Status: Temporary Relief

Currently Not Collectible (CNC) status, also called hardship status, temporarily suspends IRS collection activity when paying would create undue hardship.

The IRS determines you’re CNC if your monthly income minus allowed living expenses leaves nothing available to pay toward your tax debt.

What CNC status does:

- Stops IRS collection actions (levies, liens)

- Prevents IRS from seizing your bank accounts or garnishing wages

- Gives you time to improve your financial situation

What CNC status doesn’t do:

- Reduce your tax debt

- Stop interest and penalties from accruing

- Last indefinitely – the IRS reviews your status annually or biannually

CNC status can cause the 10-year collection statute to expire before the IRS collects the debt. If your financial situation doesn’t improve and the collection statute expires, the debt becomes uncollectible.

To qualify:

- Complete Form 433-F or 433-A showing income and expenses

- Demonstrate that paying would prevent you from meeting basic living expenses

- Provide documentation of financial hardship

The IRS may file a Notice of Federal Tax Lien even when you’re in CNC status to protect its interest in case your financial situation improves.

Penalty Abatement: Reduce or Eliminate Penalties

Penalty abatement removes IRS penalties from your account, reducing what you owe. You still owe the underlying tax and interest, but penalties can represent 25% or more of your total debt.

First-Time Abate (FTA):

Available to taxpayers with clean compliance history. If you had no penalties for the three prior tax years, filed all required returns, and paid or arranged to pay any tax due, the IRS will abate failure-to-file, failure-to-pay, and failure-to-deposit penalties for one tax year.

FTA is administrative relief – you don’t need to prove hardship or reasonable cause. Simply request it and meet the requirements.

Reasonable Cause:

The IRS abates penalties if you can prove circumstances beyond your control prevented compliance:

- Serious illness, hospitalization, or death in immediate family

- Natural disaster destroying records

- Inability to obtain records despite reasonable efforts

- Erroneous written IRS advice

- Fire, casualty, or other disturbance

You must provide documentation supporting your claim and show you made reasonable efforts to comply despite the circumstances.

Statutory Exception:

Applies when written IRS advice was erroneous, or the IRS made an error or delay in processing.

Who Qualifies for IRS Fresh Start Relief

Eligibility varies by which option you pursue. Understanding requirements before applying prevents wasted time and rejected applications.

Universal Requirements (All Options)

All required tax returns must be filed. The IRS won’t consider any relief option until you’re compliant with filing requirements. If you haven’t filed returns for the last five years, you need to file them before applying for relief.

Current year tax obligations must be met. Self-employed individuals must be current on quarterly estimated tax payments. Business owners with employees must be current on federal tax deposits.

You cannot be in an open bankruptcy proceeding. Taxpayers currently in bankruptcy must work through bankruptcy court, not IRS collection alternatives.

Income and Debt Thresholds

Streamlined Installment Agreements: Total balance owed $50,000 or less (individuals), $25,000 or less (businesses)

Offers in Compromise: No specific dollar limit, but offers work best for taxpayers with lower income and assets relative to debt

Currently Not Collectible: No dollar limit, but you must prove paying would prevent meeting basic living expenses

For self-employed taxpayers, demonstrating a 25% or greater decline in income can help qualify for certain relief options or more favorable terms.

Financial Disclosure Requirements

More complex relief options require detailed financial disclosure:

Streamlined agreements: Minimal disclosure, basic income verification

Non-streamlined agreements: Form 433-F or 433-A with complete income, expense, and asset information

Offers in compromise: Form 433-A (OIC) or 433-B (OIC) with extensive documentation including:

- Three months of bank statements

- Three months of pay stubs

- Documentation of all assets (real estate, vehicles, retirement accounts, businesses)

- Proof of expenses (lease agreements, insurance policies, utility bills)

- Tax returns for prior years

Currently Not Collectible: Form 433-F or 433-A with documentation proving financial hardship

The IRS uses national and local standard expense allowances. You can’t claim unlimited expenses – the IRS compares your claimed expenses against allowable amounts for your household size and geographic location.

How to Apply for Fresh Start Relief Options

Each relief option has its own application process and required forms.

Applying for Installment Agreements

Online application: Apply through IRS.gov using the Online Payment Agreement tool if you owe $50,000 or less

By phone: Call the number on your IRS notice to request an installment agreement

By mail: Submit Form 9465, Installment Agreement Request, with Form 433-F (if required)

For direct debit agreements, provide bank account information. Direct debit agreements have lower setup fees and higher approval rates than agreements with other payment methods.

Applying for Offer in Compromise

Pre-qualification: Use the IRS Offer in Compromise Pre-Qualifier tool to estimate if you qualify

Required forms:

- Form 656, Offer in Compromise

- Form 433-A (OIC) for individuals

- Form 433-B (OIC) for businesses

Application fee: $205 (waived for low-income taxpayers)

Initial payment:

- Lump sum offers: 20% of offer amount with application

- Periodic payment offers: First payment with application, then monthly while IRS reviews

Submit to:

Brookhaven Internal Revenue Service

Attn: Brookhaven Offer in Compromise

P.O. Box 9007

Holtsville, NY 11742-9007

Or

Memphis Internal Revenue Service

Attn: Memphis Offer in Compromise

P.O. Box 30804

AMC

Memphis, TN 38130-0804

Use certified mail with return receipt to track submission.

Applying for Currently Not Collectible Status

Call the number on your IRS notice and request hardship status, or submit:

- Form 433-F, Collection Information Statement

- Documentation of financial hardship

- Proof of income and expenses

The IRS may request additional documentation before granting CNC status.

Requesting Penalty Abatement

First-Time Abate: Call the IRS and request FTA, or write a letter requesting abatement under the First-Time Abate provisions

Reasonable Cause: Submit a detailed written explanation with supporting documentation showing circumstances that prevented compliance

Common Fresh Start Application Mistakes

Understanding what causes rejections helps you avoid them.

Applying Before You Qualify

The most common mistake is applying for relief before meeting basic eligibility requirements. If you haven’t filed all required returns, the IRS automatically rejects your application without reviewing financial information.

File all missing returns before pursuing any relief option.

Inadequate Financial Documentation

Offers in compromise fail when taxpayers don’t provide complete financial documentation. Missing bank statements, undocumented assets, or unexplained deposits trigger rejections.

The IRS can access your financial information through summons. Hiding assets or understating income results in automatic rejection plus potential civil or criminal penalties for false statements.

Unrealistic Offer Amounts

Offering far less than your reasonable collection potential guarantees rejection. Some taxpayers think they can “negotiate” like buying a car. The IRS has a specific formula for calculating RCP.

Your offer must equal or exceed what the IRS calculates as collectible. Lowball offers waste time and create skepticism about future applications.

Not Staying Current During Review

If you fall behind on current year taxes while the IRS reviews your offer or payment plan application, they’ll reject it.

File all current returns on time, make all estimated tax payments, and stay current on payroll deposits if you have employees.

Claiming Excessive Expenses

The IRS uses national and local standard allowances for living expenses. You can’t claim $3,000/month for food when the allowable amount for your household size is $800.

Claiming expenses above allowable standards triggers rejection unless you can prove the expense is necessary for health, welfare, or production of income.

Why Offers in Compromise Get Rejected

With only 30-36% acceptance rate, understanding rejection reasons is critical.

Ability to pay in full: The IRS determines you can pay through an installment agreement or your assets/income exceed the tax liability

Non-compliance: Missing tax returns, unpaid current year taxes, or failure to make required deposits

Incomplete application: Missing forms, unsigned documents, or inadequate financial disclosure

Insufficient offer amount: Your offer is less than reasonable collection potential

Lack of hardship: Your financial disclosure shows ability to pay more than offered

Default during review: Missing a payment under a periodic payment offer or failing to file current returns

Professional representation significantly improves acceptance rates. Tax attorneys and enrolled agents experienced in offer negotiations understand how to structure offers, document financial hardship, and respond to IRS inquiries effectively.

How Long Fresh Start Relief Takes

Processing times vary by option.

Streamlined Installment Agreements: Immediate to 30 days if applied online with direct debit

Non-Streamlined Installment Agreements: 30-90 days depending on complexity

Offers in Compromise: 6-24 months for complete review and decision

Currently Not Collectible: 30-90 days once financial information is submitted

Penalty Abatement: Immediate to 60 days depending on type and documentation

During review periods, the IRS generally suspends active collection but continues assessing interest and penalties.

What Happens After Approval

Approval comes with ongoing obligations.

Installment Agreements

Make payments on time every month. Missing two payments results in default and immediate resumption of collection actions.

File all future returns on time and pay any future taxes due. The agreement covers only past tax debts – you’re responsible for staying current going forward.

The IRS can modify or terminate the agreement if your financial situation significantly improves.

Offers in Compromise

Remain in compliance with all tax filing and payment obligations for five years. This means:

- File all returns by their due dates

- Pay all taxes owed for five years after acceptance

- Make all required estimated tax payments

- Stay current on payroll deposits if you have employees

If you fail to comply within five years, the IRS can revoke your offer and reinstate the full original debt minus any payments made.

Currently Not Collectible Status

File all future returns on time even if you can’t pay. The IRS reviews your financial situation annually or biannually to determine if you still qualify for hardship status.

If your financial situation improves, report it to the IRS. They’ll remove CNC status and resume collection.

Fresh Start Scams to Avoid

Many companies use “Fresh Start” in advertising to sell tax resolution services. Some are legitimate. Many are not.

Warning signs of scams:

- Guaranteeing they can settle your debt for “pennies on the dollar”

- Claiming you qualify before reviewing your financial situation

- Charging large upfront fees before doing any work

- Promising to stop IRS collection immediately

- Pressuring you to sign up quickly

- Claiming special relationships with the IRS

Legitimate tax professionals:

- Review your financial situation before recommending options

- Explain whether you qualify and why

- Charge reasonable fees for actual work performed

- Provide written engagement agreements

- Have credentials (CPA, EA, tax attorney) you can verify

You can apply for Fresh Start options yourself directly with the IRS for free. The IRS doesn’t charge for installment agreements (except small setup fees), offers in compromise (except the $205 application fee), or currently not collectible status.

Get Professional Guidance for Tax Relief

The IRS Fresh Start initiative provides legitimate pathways to resolve tax debt, but navigating the options requires understanding complex eligibility requirements, IRS procedures, and strategic considerations.

I’ve spent more than 15 years representing clients in IRS matters. I’ve negotiated offers in compromise that saved clients hundreds of thousands of dollars. I’ve also seen taxpayers lose tens of thousands pursuing the wrong relief option or applying without proper preparation.

The difference between successful tax resolution and wasted time often comes down to understanding which option fits your situation and structuring your application correctly.

If you owe back taxes and can’t pay in full, professional representation can significantly improve your outcome. An experienced tax attorney understands how the IRS evaluates financial information, what documentation satisfies their requirements, and how to respond to objections during review.

At Silver Tax Group, I provide comprehensive representation for taxpayers pursuing IRS collection alternatives. We analyze your financial situation, determine which relief options you qualify for, prepare complete applications with proper documentation, and handle all IRS communications throughout the process.

Contact Silver Tax Group today for a consultation on your tax debt situation. We’ll review your specific circumstances, explain which Fresh Start options apply to you, assess your realistic chances of approval, and develop a strategic approach to resolve your tax liability.

Because settling with the IRS isn’t about what you want to pay – it’s about what the IRS will accept based on their specific formulas and requirements. And knowing those requirements before you apply is the difference between relief and rejection.

Call us or visit our website to schedule your consultation. Stop letting tax debt control your financial future. Find out which resolution option actually works for your situation and get expert representation to navigate the process successfully.