One in five Americans fears they’ll owe the IRS this tax season.

If you’re one of them, don’t panic. There’s still time to start planning and file your tax correctly.

If you owe taxes and/or are unable to pay them, you could face a failure to pay penalty among other fines and fees.

Keep reading to learn more about the most common tax penalties and how to avoid them.

1. Failure to Pay Penalty

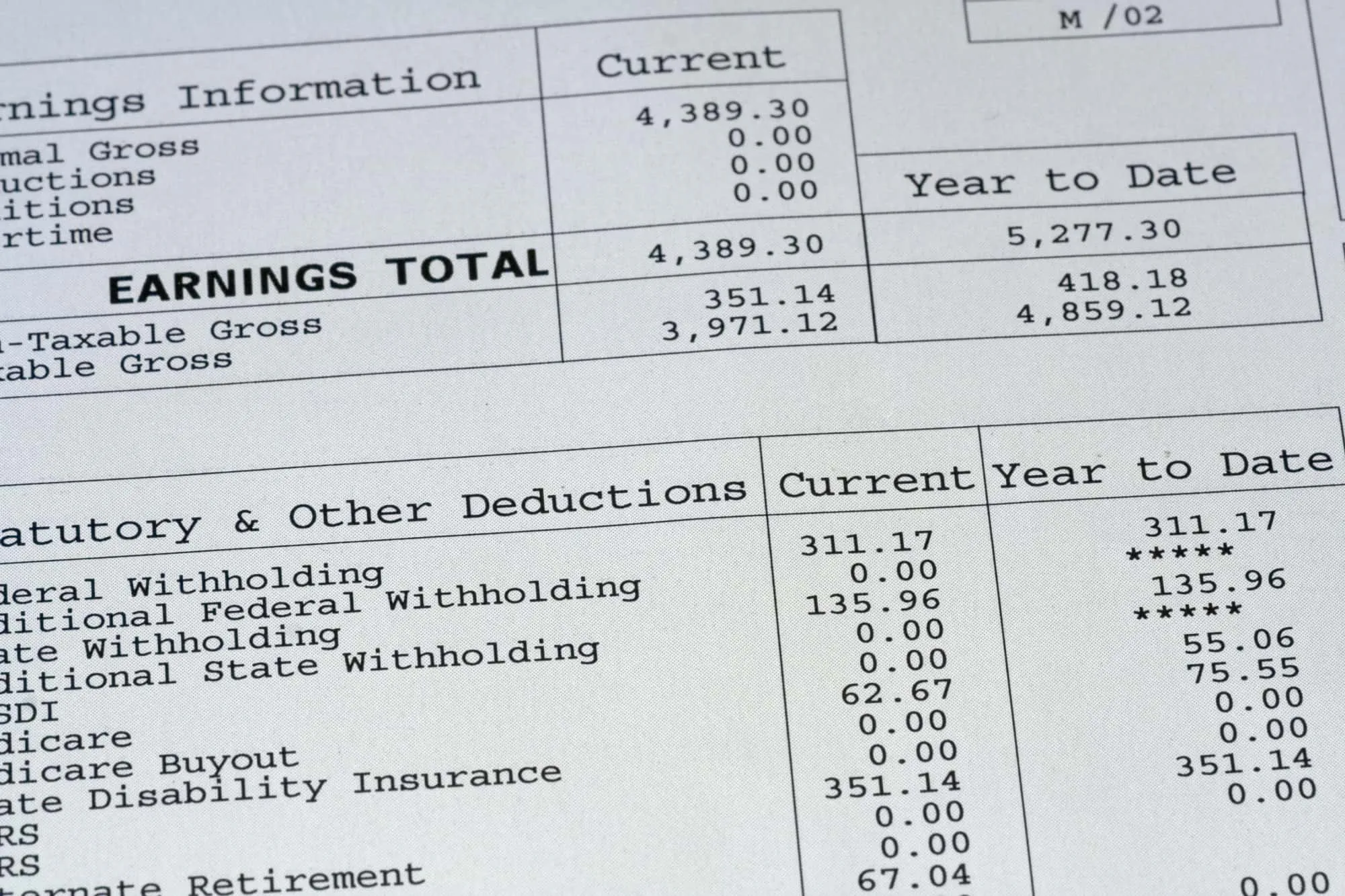

Although many taxpayers receive a refund each year, some of them will end up owing the IRS when they send in their returns. This has become increasingly common, particularly as a result of the new Tax Cuts and Job Act that was passed in December 2017.

This legislation changed the withholding tables for the IRS and the U.S. Department of Treasury. These guidelines determine how much income tax is deducted from your paycheck. After the passing of this legislation, taxpayers were supposed to adjust their W-4 forms and their withholding preferences.

Many Americans saw bigger paychecks but didn’t realize that they would be in for a surprise when they filed their taxes. According to the Government Accountability Office, 30 million people didn’t withhold the proper amount of taxes from their paychecks last tax season.

This meant that 1 in 5 taxpayers wouldn’t get a refund and might even receive a tax bill.

If you end up owing the IRS money and fail to get the taxes you owe paid by the deadline, you’ll face a failure to pay penalty. This is also called the failure to file penalty. The penalty will amount to 5% of the amount you owe per month or partial month your return and payment are late.

If you don’t pay soon enough, the penalty amount will increase. You could end up with a penalty amount of up to 25% of the amount you owe.

You might be thinking that being a little late won’t hurt but the IRS takes its deadlines very seriously. In fact, if your return is more than 60 days late you’ll face a minimum penalty of $135 or 100% of the amount you owe, whichever is less.

2. Late Payment Penalty

![]()

The late payment penalty goes hand in hand with the failure to pay penalty. If you don’t get a refund and actually end up owing a tax bill, you better pay on time if you don’t want to face hefty penalties.

If you don’t pay your tax bill by the filing deadline, you’ll get slapped with a 0.5% penalty for every month or partial month your bill remains unpaid. This penalty has a maximum amount of 25%.

Keep in mind that this penalty could be in addition to the failure to file penalty. If both of these penalties apply to you, your maximum penalty won’t exceed 5% per month. Nonetheless, we are talking about a lot of money to lose, especially if you are already struggling.

3. RMD Penalty

![]()

Unfortunately, the money stored in your retirement savings account, be it a 401(k) or traditional IRA can’t keep growing forever. Once you reach age 70 1/2 you have to start making the required minimum distributions.

Your account is designed to help you save and build a retirement fund, but once you reach the age of retirement, you’re expected to be using the funds for survival. A required minimum distribution or RMD is the mandatory minimum amount you must withdraw from your retirement account.

The exact amount you have to withdraw depends on your account balance as well as your age and life expectancy. There are a lot of rules surrounding RMDs so it’s important to be careful to avoid tax penalties.

Some people have trouble taking their required minimum distribution because they don’t need the money and the withdrawal triggers taxes. If you’re in this situation, don’t even think about failing to take your scheduled withdrawals.

The consequences for not making a withdrawal are far greater than the taxes you’ll pay by withdrawing. In fact, the IRS will fine you 50% of whatever amount you failed to withdraw as a penalty.

For example, if your required minimum distribution for a given year is $10,000 and you fail to take it, you’ll automatically lose $5,000.

You have to make your first withdrawal by April 1st of the year following the calendar year where you turn 70 1/2. All RMDs after this are due by the last day in the calendar year.

4. Early Retirement Plan Withdrawl Penalty

![]()

When you save for retirement using a 401(k) or a traditional IRA, you benefit when it comes to tax time. The money you contribute to these accounts is tax-free. This means your taxable income is lower every year you contribute and you save money on your tax bill.

In exchange for these tax benefits, you have to truly save this money for retirement. If you withdraw money from these types of accounts before you turn 59 1/2, you’ll face a tax penalty. This is usually a 10% penalty on the amount you withdraw early.

Fortunately, there are some exceptions that can spare you an early withdrawal penalty. The IRS allows you to tap into your account early if you are using the funds to purchase your first home or pursue higher education.

You can also use the funds if you become permanently disabled or you incur medical costs above 10% of your adjusted gross income for a year. If you’re 55 or older and you no longer work for the employer that sponsors your plan, you can access your account early without incurring a penalty.

If none of these circumstances apply and you withdraw money from your account, you can face significant penalties. Avoid these penalties by talking to your tax attorney before making any withdrawals.

If you do need to make an early withdrawal, you better be prepared to pay the penalty. You’ll also have to pay taxes on the amount you withdraw because the money was deposited into your account tax-free.

How to Avoid Tax Penalties

Now that you have a better idea of some of the most common penalties faced by taxpayers, let’s take a look at how to avoid them. When it comes to taxes, prevention is worth more than a cure. Planning ahead is the best way to avoid tax fraud penalties.

Be Prepared by Filing Early

If you know you’re going to owe taxes or suspect you might, it’s in your best interest to file as soon as possible. By filing early, you can estimate your tax liability long before payment is due.

The earlier you determine what you’re going to owe, the longer you’ll have to get the money together. Whatever balance you owe isn’t due until April 15th. If you don’t end up owing and instead get a refund, you’ll get that money sooner.

Doing your taxes early means you’ll get them over with whether or not you end up owing.

If you owe taxes and don’t file, you’ll get stuck with a “failure to file” penalty. This penalty is 10 times greater than the failure to pay penalty when you do file but don’t pay what you owe.

The bottom line here is that even if you can’t pay what you owe, you’ll get in more trouble by failing to even file a return. You have options when it comes to working out payment arrangements but the IRS doesn’t look kindly on those who fail to even file.

Request an Extension

If for some reason you aren’t able to file your return by the deadline to file, you can request an extension. The IRS is generally willing to grant a request for an extension and give you until October 15th to file your tax return.

The catch here is that an extension to file is not an extension to pay. If you owe taxes, they are still due by the April 15th deadline.

To avoid tax penalties, make sure to pay your bill before the April 15th due date. The IRS doesn’t want to wait until October to receive the money they are owed. The deadline to file an extension is April 15th.

Negotiate a Payment Plan

If you owe money to the IRS and can’t afford to pay what you owe, there are some things you can do. Simply ignoring what you owe is the worst thing you can do as penalties and fines will continue to add up. Your best course of action is to communicate with the IRS as soon as you know you can’t pay.

There are several options for paying off your debt that will help you avoid penalties. The first option is the IRS’s short term payment plan. This plan allows you to make monthly payments to pay back your debt.

The catch? You have to pay back your entire balance within 120 days. You’ll still owe interest and penalties during your payback period but you won’t be subject to any additional fees.

If you owe a larger amount, you might be able to qualify for a long term payment plan. With one of these plans, you’ll have longer than 120 days to pay what you owe. You will have to pay application fees though.

Proving Financial Hardship

If paying what you owe will result in significant financial hardship for you, you may be eligible for the Offer in Compromise program. If you qualify, you can make an offer in compromise to the IRS offering to pay less than what you owe.

Only taxpayers facing serious financial hardship will qualify. The IRS will accept your offer if it is equal to the amount they can reasonably expect to collect from you given your financial situation. The IRS recommends taxpayers explore other options before making an offer in compromise.

If the IRS determines that you can’t make any payments towards your tax debt, it will sometimes temporarily delay collections activities until your finances improve. In this situation, you’ll still be charged interest on what you owe.

Furthermore, the IRS may file a lien against your property to protect their interest in your assets. You may be able to have certain penalties waived if you’ve paid a certain percentage of your tax liability for the previous year.

Consult a Tax Professional

Americans are notoriously uneducated about taxes. One of the best things you can do to avoid unexpected tax liabilities and penalties is to take charge of your finances.

If you know you owe the IRS or you suspect you will owe, talk to a tax professional now. Do some research on your own so you know what you want to ask your tax attorney.

It’s understandable to not fully understand your tax bracket and the impact of new legislation on your tax status. But to avoid penalties, you need to make yourself aware.

If you didn’t adjust your withholding status, if you’re in a state with high taxes, if you usually write off work expenses, or if you have a large salary, you’re more likely to deal with complex returns. It’s important to know what you might end up owing as soon as possible to avoid penalties.

Working with a tax attorney is the best way to get yourself into a better position for tax filing season. Your tax attorney will also help you understand the rules you need to know about your retirement accounts to avoid penalties related to them.

Contact Silver Tax Group Today

![]()

If you’re facing a failure to pay penalty or any other tax issue, we are here to help. You can avoid additional penalties and fees by acting now.

Don’t ignore the IRS.

Contact us today and let us help you resolve your tax debt and put your mind at ease.