Most OIC applications I see come back for the same handful of reasons. Wrong form version. Missing bank statements. An offer amount that doesn’t match the financial statements. And every single time, the person filing it thought they had everything right.

Form 656-B is the IRS’s Offer in Compromise application booklet. The whole application kit lives inside one PDF. You’ve got Form 656 (the actual offer), the 433-A (OIC) financial statement for individuals, the 433-B (OIC) for businesses, plus worksheets, instructions, and a submission checklist. Everything in one download. The IRS revised it in April 2025, and if you submit the old version, they send it back. No review. No exceptions.

I’ve filed over 128 of these applications since 2020. The process isn’t complicated if you understand what the IRS is looking for. The problem is that the booklet is 30+ pages, the instructions assume you already know tax terminology, and one miscalculation on your Reasonable Collection Potential changes your entire minimum offer amount. This guide breaks the form down section by section so you know exactly what goes where, what the IRS checks first, and where people get tripped up.

Want to know if you qualify before filing? Use our free Offer in Compromise calculator to estimate your offer amount.

What’s Actually Inside Form 656-B?

People assume 656-B is a form. It’s actually a booklet the IRS puts together with every document you need to apply for an Offer in Compromise. Think of it as an all-in-one application kit.

Click here for the most up-to-date version of the IRS Form 656-b, Offer in Compromise PDF.

Here’s what you’ll find when you open it:

The IRS updated Forms 433-A and 433-B in April 2025. If you downloaded the booklet before then, your forms are outdated. The IRS will return the whole package, and your collection clock keeps ticking while you start over.

Form 656 vs. Form 656-L: Pick the Wrong One and You’re Starting Over

There are two versions of Form 656. Filing the wrong one doesn’t get you redirected. It gets you sent back to square one.

Form 656 (the one inside the 656-B booklet) is for the two most common types of offers. Doubt as to Collectibility means you agree you owe the money, but you can’t pay it. That’s the vast majority of cases I work on. Effective Tax Administration means you technically could pay, but doing so would wreck you financially or would be genuinely unfair given your circumstances. Less common, but it happens.

Form 656-L is completely separate. It’s for Doubt as to Liability, which means you’re arguing you don’t actually owe what the IRS says you owe. Different form, different rules, different documentation. And it’s not inside the 656-B booklet at all.

I’ve had people walk into my office after submitting a Doubt as to Liability offer when their real issue was Doubt as to Collectibility. The IRS didn’t fix it for them. They returned the application, kept the processing time, and the person had to start from zero. If you’re not 100% sure which one applies, that’s worth a phone call to a tax attorney before filing.

Before You Touch the Application, Check These Four Things

The IRS has a short list of prerequisites, and they don’t bend on any of them. If you’re missing even one, they’ll send your application back before an examiner ever looks at it.

All your tax returns need to be filed. Every year. No gaps. If you have unfiled returns sitting out there, take care of those first. The IRS will check, and they won’t review your offer until every return is accounted for.

Estimated tax payments for this year need to be current. W-2 employees, your withholding covers this. Self-employed? Your quarterly estimated payments need to be paid through the current quarter. Not last quarter. This quarter.

Employers need current federal tax deposits. That means the current quarter and the two before it. Payroll taxes, FICA, all of it.

You can’t have an active bankruptcy case. If you’re in an open bankruptcy proceeding, the IRS won’t consider your offer. Period. Resolve the bankruptcy first.

Here’s what frustrates me about this part: people spend hours filling out the application, scrape together the $205 fee, mail it in, and get the whole thing returned because they had one unfiled return from 2019 they forgot about. Check every box on this list before you invest the time. The IRS keeps your initial payment even on returned applications (they apply it to your balance), so that money is gone whether they review your offer or not.

Walking Through Form 656, Section by Section

The form has nine sections. If you’re an individual, you fill out Section 1 and Sections 3 through 9. Businesses (corporations, LLCs, partnerships) fill out Sections 2 through 9. Let me walk you through what matters in each one.

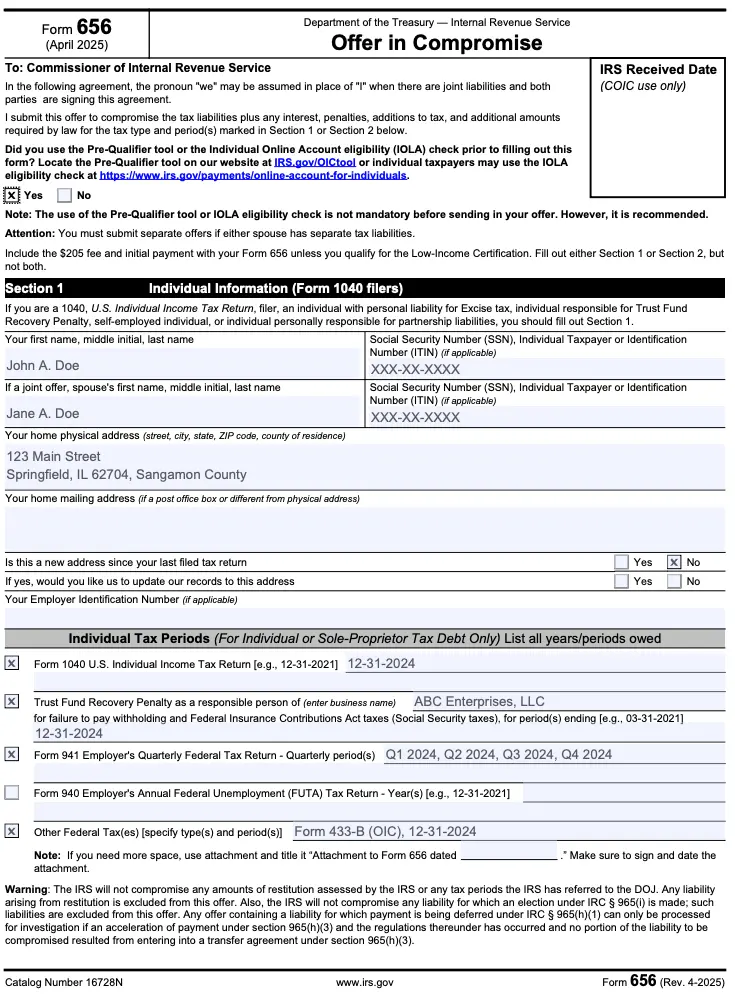

Section 1: Your Info and the Low-Income Certification

Name, Social Security number, address. Standard stuff. But there’s a box here that saves a lot of people real money, and most don’t know about it.

I’ve worked with people who drained their last $400 to cover the fee and initial payment when they didn’t have to. The income thresholds are printed right on the form. Check them before you write a check.

Section 1 pt. 2: Low-Income Certification

This is the part that can save you the $205 application fee and all payments while the IRS reviews your offer. Most people skip past it. Don’t.

If your adjusted gross income (from your last filed 1040) falls at or below 250% of the federal poverty guidelines for your family size and state, you qualify for low-income certification. That means no $205 application fee and no payments while the IRS reviews your offer. Zero. Here are the current numbers:

Two ways to qualify: Check the first box if your AGI from your most recent tax return falls at or below the number for your family size. Check the second box if your household’s gross monthly income from Form 433-A (OIC) multiplied by 12 falls at or below the threshold instead. You only need to meet one.

What you get if you qualify: No $205 application fee. No initial payment with your offer. No monthly payments while the IRS reviews your case. The IRS verifies your income themselves, so don’t guess. Pull your most recent 1040 and check before you file.

Who doesn’t qualify: Businesses other than sole proprietorships, and offers filed on behalf of a deceased individual. Those still owe the full fee and payment regardless of income.

One thing to watch for: If you do qualify, don’t include any payment with your offer. The form says it clearly, but people send checks anyway out of habit. Those payments won’t be returned, and the IRS applies them to your tax balance whether you wanted them to or not.

Section 2: Business Information

This is for business entities only. Your EIN, business name, address, and entity type go here. If you’re a sole proprietor, skip this entirely. Everything about your business goes on Form 433-A (OIC) with your personal information.

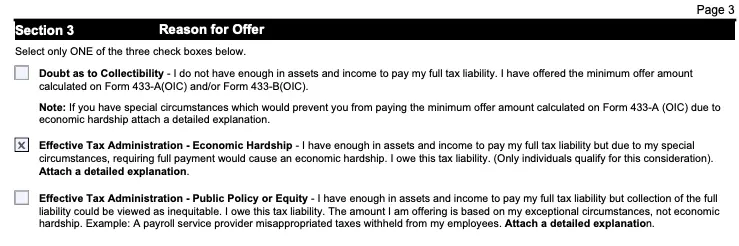

Section 3: Why the IRS Should Take Less Than You Owe

You pick one of three boxes. Only one.

Doubt as to Collectibility. You agree you owe the tax, but you can’t pay it. Most common option by far. Your offer amount needs to match or exceed the minimum from your 433-A (OIC) or 433-B (OIC). If you can’t pay even that minimum, attach a written explanation of why.

Effective Tax Administration, Economic Hardship. You could technically pay in full, but doing so would leave you unable to cover basic living expenses or medical care. Only available to individuals. Attach a detailed explanation.

Effective Tax Administration, Public Policy or Equity. You can afford to pay, but full collection would be genuinely unfair given exceptional circumstances. The IRS’s own example: a payroll provider who mishandled your employees’ withholding. If your situation isn’t that unusual, this probably isn’t your box. Attach a detailed explanation.

How to Write the Attached Explanation

For all three options, the IRS wants a separate written statement. Without one, you’re giving the examiner a checked box with no context. Keep it to one page and hit three things:

What happened and when. “In March 2024, I was laid off. I found new work in June 2024 at $30,000 less than my previous salary.”

How it affected your finances. “During three months of unemployment, I spent $14,000 in savings on mortgage payments and my spouse’s medical bills.”

Where that leaves you today. “My current monthly income is $3,800. After allowable expenses, I have $200 in disposable income. Paying $47,000 in full isn’t possible within the collection statute.”

Dates, dollar amounts, specific events. That’s it. The explanation needs to match the numbers on your 433-A or 433-B. If your statement says you were unemployed for three months but your financial forms show steady income during that period, the examiner will catch it.

Label the page “Section 3 – Detailed Explanation” at the top with your name and SSN. Staple it behind your Form 656, or upload it as a separate PDF if you’re filing through your IRS Online Account.

Section 4: Payment Terms

You have two options, and each one changes your minimum offer amount.

Option 1: Lump Sum Cash. Send 20% of your offer upfront. Pay the rest in 5 or fewer payments within 5 months if accepted. The IRS multiplies your monthly disposable income by 12 to calculate your minimum offer. Lump sum almost always produces a lower offer amount, but you need the 20% in hand.

Option 2: Periodic Payment. Send the first month’s payment upfront. Keep paying monthly while the IRS reviews (6-12 months typically). If accepted, continue until paid off, up to 24 months total. The IRS multiplies your monthly disposable income by 24. Periodic payments require less cash upfront, but the total offer is higher and you’re making payments for months while you wait on a decision.

If you miss one periodic payment while the IRS is reviewing your offer, they return the entire application. No appeal. Start over. I’ve seen it happen over $150.

If you can pull together the 20%, go lump sum. Lower offer, shorter process, no monthly payment hanging over you.

Sections 5-6: Where Your Money Goes and Where It Comes From

Section 5 lets you tell the IRS which tax years to apply your payments toward. If you skip this, they apply the money wherever they want. Your call.

Section 6 asks where the money is coming from. Be honest. If your parents are giving you the lump sum, say so. If you’re borrowing it, say that. The IRS will investigate your finances during the review, and unexplained deposits in your bank account raise questions you don’t want to answer later.

Section 7: The Fine Print That Can Bite You in Year Three

This is the terms and conditions section. Most people skim it. That’s a mistake.

A few things buried in here that you need to know:

The IRS can still file a federal tax lien while your offer is pending. Collection activity stops (no levies, no garnishments), but liens are fair game. Your payments and the $205 fee are non-refundable once the IRS starts investigating your offer. If they don’t make a decision within 24 months of receiving your offer at the right processing center, your offer is automatically accepted. That almost never happens, but it’s worth knowing.

Now here’s the big one. After acceptance, you have to file every tax return on time and pay every dollar of tax you owe for the next 5 years. Miss a filing deadline in year three? The IRS can default the entire agreement and reinstate your original balance. All of it. I’ve seen this happen to people who got their OIC accepted, felt the relief, then got sloppy with an extension they forgot to file. Five years is a long time to stay perfect. Plan for it.

Sections 8-9: Signatures

Sign and date the form. If it’s a joint offer, both spouses sign. If a tax attorney or CPA prepared it, they fill out Section 9.

Sounds like the easiest part, right? You’d be surprised how many applications come back because someone forgot to sign. Or one spouse signed and the other didn’t. Don’t let a missing signature waste 3 months of your time.

Form 433-A and 433-B: Where the IRS Decides If Your Offer Is Realistic

Your financial statements are the heart of the application. The IRS uses them to calculate your Reasonable Collection Potential (RCP), and that number determines the minimum offer they’ll accept.

These forms ask about everything. Bank balances, vehicle values, real estate equity, investment accounts, retirement funds, and (as of the April 2025 revision) digital assets. That includes cryptocurrency, NFTs, and stablecoins. The IRS added those categories specifically, and leaving them blank when you own crypto is a fast way to get flagged.

Here’s the basic formula the IRS uses:

Minimum Offer = Quick-Sale Value of Your Assets + (Monthly Disposable Income × 12 or 24)

Quick-sale value means roughly 80% of fair market value, minus any loans or liens. Monthly disposable income is your total household income minus what the IRS allows for living expenses. They use their own published expense standards (National Standards for food and personal care, Local Standards for housing and transportation), not what you actually spend.

Three places where I see people get the math wrong every time:

Vehicle equity. The IRS takes current market value, multiplies it by 0.8, and subtracts the loan balance. If you owe more than 80% of the car’s value, the equity is zero. Don’t put negative numbers here, or the IRS will flag it.

Living expenses. You can’t claim your actual mortgage payment if it exceeds the IRS’s Local Standard for your county. If your housing costs run higher than what the IRS allows, you need documented proof of why the overage is necessary. Medical conditions, disability, court-ordered obligations. Without documentation, the examiner uses the standard amount, and your disposable income (and your minimum offer) goes up.

Future income. The IRS looks at your earning history and what you could earn going forward. If you quit a $90,000 job six months before filing and now report $40,000 in income, the examiner will notice that gap.

What Goes in the Envelope (or the Online Submission)

The back page of the 656-B booklet has a checklist. Use it. I’m serious. Tape it to your desk and check every item off before you seal anything.

Here’s what the IRS needs in the package:

In 2026, individual taxpayers can now file through their IRS Individual Online Account at IRS.gov. You can check eligibility, calculate a preliminary offer amount, and submit electronically. Businesses still have to file by mail.

7 Mistakes That Get Applications Returned (I’ve Seen All of Them)

After 228+ OIC filings in the past couple years, these are the errors I see over and over from people who tried it themselves before calling us:

1. Outdated forms. The IRS rewrote Forms 433-A and 433-B in April 2025. Grab your copy and check the bottom corner. If it doesn’t say “Rev. 4-2025,” it’s the old version, and the IRS will send the whole package back without reading a word.

2. Unfiled returns. Even one. Doesn’t matter if it’s a year you think you didn’t owe anything. If a return is required and it’s not filed, the IRS rejects the application at the door.

3. Offering below your RCP without explaining why. If your financial statements show the IRS could realistically collect $8,000, and you offer $3,000, that’s a rejection. Your offer needs to meet or exceed your Reasonable Collection Potential unless you can document special circumstances on the form. “I can’t afford it” isn’t a special circumstance. A documented medical condition that prevents you from working is.

4. Gaps in the financial documentation. Missing bank statements. No vehicle values listed. Skipping the asset section because you think you don’t own anything worth reporting. The IRS doesn’t read blank spaces as “nothing to report.” They read them as “what are you hiding?”

5. Leaving digital assets off the form. The April 2025 revision added specific fields for cryptocurrency, NFTs, and stablecoins. If you own any and don’t disclose them, your application is incomplete. The IRS added those fields for a reason.

6. Missing a periodic payment during the review. Choose the periodic payment option, miss one installment during the 6-12 month review, and the IRS returns your offer. You don’t get an appeal. You don’t get a warning. You start the entire process over with a new fee and new application.

7. Unsigned forms. Or only one spouse signing a joint offer. I know. It sounds too simple to mess up. But I’ve personally seen applications come back for exactly this reason. Twice in the same month, once.

Should You File This Yourself or Get an Attorney?

You’re allowed to do it yourself. The IRS publishes everything for free, and their Pre-Qualifier tool on IRS.gov will tell you if you’re likely eligible. For a simple case (one tax year, W-2 income, no real assets, clear financial hardship), you might be fine on your own.

But I’ll be straight with you about where the DIY approach breaks down.

If you have multiple tax years involved, self-employment income, a business with assets, real estate, or a situation where the IRS could argue you should sell something to pay your debt, the math gets complicated fast. One wrong number on the 433-A changes your minimum offer by thousands. And you won’t know it’s wrong until the IRS rejects you 8 months later.

Consider that when you file an OIC, you’re handing the IRS a complete financial x-ray. Every bank account, asset, and income source. If the offer gets rejected, the IRS still has all of that information, and they can (and do) use it to pursue collection more aggressively than before you applied. Filing a weak offer can actually make your situation worse.

At Silver Tax Group, our tax attorneys review your full financial picture before we recommend anything. Sometimes an installment agreement or Currently Not Collectible status is the better move. We tell you that before you spend the $205 and 6-12 months waiting on an answer that was never going to be yes.

Form 656-B Frequently Asked Questions

How much does it cost to file an Offer in Compromise?

The application fee is $205. You also owe an initial payment: 20% of the offer for lump sum, or the first monthly installment for periodic payments. If your AGI falls at or below 250% of the federal poverty level for your family size, the IRS waives both the fee and all payments during review.

How long does the IRS take to review an OIC?

They say up to 24 months. Most cases I’ve worked on get a decision within 6-12 months. If the IRS doesn’t issue a decision within 24 months of receiving your offer at the correct processing center, the offer is automatically accepted. I’ve never seen that happen, but the rule exists.

What happens to IRS collection while my offer is pending?

Most collection activity stops. No wage garnishments, no bank levies, no property seizures while the offer is under review. The catch: the IRS can still file a federal tax lien. And if you had an existing installment agreement, you don’t need to keep making those payments while the offer is pending.

Can I file an Offer in Compromise online?

Individual taxpayers can, yes. The IRS now lets you check eligibility and submit through your Individual Online Account at IRS.gov. Businesses still have to go the paper route and mail everything using the addresses in the 656-B booklet.

What if my OIC gets rejected?

You get 30 days from the rejection letter to file an appeal using Form 13711. The IRS Independent Office of Appeals reviews your case with fresh eyes. Miss that 30-day window, though, and you’re submitting a brand new application with a new fee and new initial payment. Don’t miss it.

Do I need separate forms for personal and business tax debt?

Yes. Individual tax debt and business tax debt (corporations, partnerships, LLCs) each need their own Form 656, their own $205 fee, and their own initial payment. Sole proprietor debts go on the individual Form 656, so you don’t need a separate filing for those.

Get This Right the First Time

The OIC process takes 6-12 months when everything goes well. Filing an incomplete application, or one with a miscalculated offer amount, adds months to that timeline. You lose the fee. You lose the initial payment. And you’re back at the starting line with the IRS still holding your financial information from the first attempt.

If you’re thinking about an Offer in Compromise, call us at 855-900-1040 for a free consultation. Our tax attorneys run the RCP calculation, review your full financial situation, and tell you whether an OIC, installment agreement, or another path gives you the best result. We’ve reduced over $5 million in tax debt so far in 2026, and we’ll be straight with you about what’s realistic. No promises we can’t keep.