Americans owed $114 billion in unpaid taxes as of 2020. That number isn’t shrinking – it’s growing every day as interest compounds and penalties stack up like cordwood.

So when someone whispers about “IRS debt forgiveness” – maybe it’s your accountant, maybe it’s a late-night TV commercial promising to “wipe out your tax debt for pennies” – you listen. Because if you’re drowning in tax debt, forgiveness sounds like the life preserver you’ve been searching for.

Here’s what’s driving me absolutely nuts about this topic: the internet is full of garbage information about IRS debt forgiveness. Half of it’s outright lies designed to separate desperate people from their money. The other half is so buried in legal jargon that you need a decoder ring to understand it.

After handling tax debt cases since 2008 – back when the economy crashed and everyone was scrambling for relief – I can tell you this: IRS debt forgiveness is real. But it’s not what most people think it is.

The IRS doesn’t forgive debt because they feel sorry for you. They don’t have a magic “one-time forgiveness program” that wipes slates clean for anyone who asks nicely. And they sure as hell don’t care about your sob story unless it fits into very specific legal categories.

But they do have legitimate programs that can eliminate or significantly reduce tax debt. The trick is understanding what’s actually available and whether you qualify.

Today, you’ll learn:

- What IRS debt forgiveness really means and the legal mechanisms the IRS uses to compromise or eliminate debt

- 8 forgiveness options that actually exist

- How to spot IRS debt forgiveness scams

- IRS qualification requirements

- When professional help is worth the cost

What IRS Debt Forgiveness Actually Means

Here’s the truth most people don’t understand: the IRS doesn’t “forgive” debt out of kindness. They eliminate or reduce debt when it makes financial sense for the government.

Think about it from their perspective. They’re a collection agency with extraordinary legal powers. They can garnish wages without court orders, seize bank accounts, and put liens on property. Why would they voluntarily accept less money?

Three reasons the IRS actually compromises debt

1. Collection is impossible – You legitimately cannot pay the full amount within their collection timeframe, and pursuing collection would cost more than they’d recover.

2. The assessment is wrong – The tax calculation has errors, or you have valid legal defenses against the liability.

3. Collection would be unfair – Forcing payment would violate basic principles of effective tax administration or cause genuine economic hardship.

That’s it. No other reasons matter. Your financial struggles, family problems, job loss, or medical bills only matter if they fit into these three categories.

The real IRS debt forgiveness programs:

- Offer in Compromise (settlement for less than owed)

- 10-year statute of limitations (debt expires after collection period)

- Currently Not Collectible status (temporary collection suspension)

- Penalty abatement (removal of penalties, not underlying tax)

- Installment agreements (payment plans, not debt reduction)

- Innocent spouse relief (relief from spouse’s tax debt)

- Insolvency exclusion (for specific circumstances)

- Bankruptcy discharge (limited situations)

Notice what’s missing? A general “debt forgiveness program” that helps anyone who applies.

8 Real IRS Debt Forgiveness Programs

1. The 10-Year Rule: Your Best Shot at Real Forgiveness

Here’s the one form of debt forgiveness that actually works for many people: the Collection Statute Expiration Date (CSED).

The IRS has 10 years from the date your tax is assessed to collect it. After that, the debt legally expires. No more collection actions, no more enforcement, no more interest. It’s gone.

Sounds simple, right? It’s not.

First problem: When does the clock start?

Not when you owe the tax – when the IRS officially assesses it. If you filed your 2020 return in 2023, your 10-year clock started in 2023, not 2020.

Second problem: The clock can pause.

Every time you take certain actions, the collection clock stops. These include:

- Filing bankruptcy

- Submitting an Offer in Compromise

- Requesting collection due process hearings

- Leaving the country for 6+ months

- Filing appeals or lawsuits

I’ve seen 10-year periods stretch to 15 years because taxpayers kept “cooperating” with the IRS without understanding they were giving away time.

Third problem: The IRS doesn’t announce when time’s up.

When your CSED passes, you need to request formal documentation that the debt is uncollectible. Otherwise, liens stay in place and you remain stuck.

Fourth problem: Collection gets aggressive near the deadline.

The closer you get to your CSED, the harder the IRS pushes. They know time’s running out, so enforcement actions accelerate.

Who benefits from the 10-year rule:

- People with large debts and limited ability to pay

- Those who can avoid tolling events during the collection period

- Taxpayers whose financial situation won’t improve significantly

Who shouldn’t count on it:

- People who can afford reasonable payment plans

- Those likely to file bankruptcy, appeals, or other actions that pause the clock

- Taxpayers with assets the IRS can easily seize

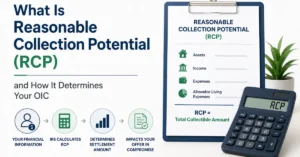

2. Offer in Compromise: Settlement Reality vs. Marketing Fantasy

An Offer in Compromise lets you settle tax debt for less than you owe – but only if you meet strict qualification criteria.

How it really works: The IRS calculates your “reasonable collection potential” – what they could realistically collect from you over time. Your offer needs to equal or exceed this amount, or you need compelling reasons why it shouldn’t.

Reasonable collection potential includes:

- Asset equity (house, cars, accounts, investments)

- Future income potential (disposable income over 12-24 months)

- Both present and future collection possibilities

Example of a realistic offer: You owe $75,000 in taxes. Your assets have $15,000 in equity. Your monthly disposable income is $500. For a lump-sum offer: $15,000 + ($500 × 12) = $21,000 minimum offer. The IRS might accept $21,000-$25,000.

Example of a rejected offer: Same situation, but you offer $5,000. Rejected immediately – your reasonable collection potential is much higher.

Two payment structures to choose from

Lump Sum Cash Offer:

- 20% down payment with application

- Balance paid within 5 payments

- IRS calculates based on 12 months of future income

- Faster processing (6-9 months)

- Often results in lower total payment

Periodic Payment Offer:

- First monthly payment with application

- Continue monthly payments during consideration period

- IRS calculates based on 24 months of future income

- Longer processing (9-12 months)

- Higher total settlement but easier on cash flow

The forms that determine your fate

Form 656 – Your actual offer to the IRS. This is where you state your offer amount and payment terms

Form 433-A (OIC) – Complete financial disclosure of every asset, debt, income source, and expense. One error or omission kills your application

Who qualifies for OIC

- People whose assets and income cannot support their tax debt

- Those facing genuine economic hardship

- Taxpayers with disputed liability issues

- People near retirement with limited earning potential

Who doesn’t qualify

- Anyone who can afford an installment agreement

- People with significant assets they’re unwilling to liquidate

- Those trying to avoid paying legitimate taxes they can afford

- Anyone in open bankruptcy proceedings

- Taxpayers with unfiled returns

The application reality

- $205 application fee (waived for low-income taxpayers)

- 6-24 month evaluation period depending on payment type

- Comprehensive financial disclosure required

- About 40% acceptance rate for properly prepared DIY applications

- 85% acceptance rate with professional representation

- 60% rejection rate overall, often for inadequate offer amounts

- Must remain compliant for 5 years after acceptance

- Federal tax liens remain until offer amount is paid in full

Critical calculation tip: Before wasting your application fee, calculate your reasonable collection potential. If you can’t offer at least that amount, save your money and pursue a payment plan instead.

3. Currently Not Collectible: Temporary Relief That Actually Helps

If you genuinely cannot pay anything right now, Currently Not Collectible (CNC) status stops collection actions without requiring payments.

How it works: You prove to the IRS that collecting would prevent you from meeting basic living expenses. They suspend collection activities until your financial situation improves.

Benefits:

- Collection actions stop immediately

- No required monthly payments

- Interest and penalties continue accruing, but slowly

- Gives you time to improve your situation

Requirements:

- Complete financial disclosure

- Proof that payment would create hardship

- Regular status reviews by the IRS

Who it helps:

- People temporarily unemployed or underemployed

- Those with serious medical issues affecting income

- Elderly taxpayers on fixed incomes

- Anyone facing genuine financial crisis

The catch: Your debt doesn’t disappear. When your situation improves, collection resumes. But CNC can buy valuable time while you get back on your feet.

4. First-Time Penalty Abatement: The Easy Win Most People Miss

This is the most underutilized form of debt relief available. If you’ve been compliant for three years before your first penalty, the IRS will abate penalties for one tax year.

Requirements:

- Filed all required returns (or extensions)

- Paid all taxes owed (or arranged payment plans)

- No penalties in the three years prior to the penalty year

What it covers:

- Failure to file penalties

- Failure to pay penalties

- Failure to deposit penalties (for businesses)

What it doesn’t cover:

- Accuracy-related penalties

Fraud penalties - The underlying tax debt

How to request it:

- Call the IRS directly (they’ll often approve over the phone)

- Submit written request with supporting documentation

- Include it as part of a comprehensive resolution strategy

Why people miss it: Most taxpayers don’t know it exists. Tax resolution companies don’t promote it because there’s no big fee involved. But it can eliminate thousands in penalties with a simple request.

5. Installment Agreements: Not Forgiveness, But Manageable Relief

Payment plans don’t eliminate debt, but they make it manageable and stop collection actions.

Streamlined installment agreements (for debts under $50,000):

- Up to 6 years to pay

- Minimal financial disclosure required

- Setup fees from $31-$225

- Direct debit options reduce costs

Standard installment agreements (for larger debts):

- Comprehensive financial analysis required

- Payment based on your ability to pay, not the debt amount

- Can extend beyond 6 years

- Subject to annual review

Partial payment installment agreements:

- For people who can’t pay the full debt within the collection period

- Payments based on disposable income

- Remaining balance forgiven when collection statute expires

- Combines payment plan with eventual forgiveness

Who benefits:

- People who can afford monthly payments but need time

- Those who want to avoid more aggressive collection actions

- Taxpayers with steady income and reasonable expenses

6. Bankruptcy: When It Actually Helps with Tax Debt

Contrary to popular belief, some tax debts can be discharged in bankruptcy – but the rules are strict.

Tax debt can be discharged if:

- The tax return was due at least 3 years ago

- You filed the return at least 2 years ago

- The tax was assessed at least 240 days ago

- You didn’t commit fraud or willful evasion

- Chapter 7: Eligible tax debts are completely discharged

- Chapter 13: You pay what you can afford over 3-5 years, remainder is discharged

What bankruptcy doesn’t help:

- Recent tax debts

- Payroll taxes for business owners

- Fraud penalties

- Tax debts from unfiled returns

When to consider it:

- You have significant non-tax debt too

- Your tax debt meets the discharge requirements

- Other resolution options aren’t viable

7. Innocent Spouse Relief: When Your Partner's Tax Problems Aren't Yours

If you’re facing tax debt because of your spouse’s actions – or former spouse’s actions – innocent spouse relief might eliminate your responsibility entirely.

How it works: The IRS can hold you responsible for taxes owed on joint returns, even if the debt resulted entirely from your spouse’s unreported income or improper deductions. Innocent spouse relief provides an escape route when that’s unfair.

Three types of relief:

1. Classic innocent spouse relief

- There’s an understatement of tax on your joint return

- The understatement is attributable to your spouse’s erroneous items

- You didn’t know and had no reason to know about the understatement

- It would be inequitable to hold you liable

2. Separation of liability relief

- You’re divorced, legally separated, or haven’t lived with your spouse for 12+ months

- You elect to separate liability for the joint return

- You didn’t know about the items causing the tax debt

3. Equitable relief

- You don’t qualify for the other two types, but holding you liable would be unfair

- Covers situations involving underpayments, not just understatements

Real-world example: Your ex-husband ran a cash business and didn’t report $80,000 in income on your joint return. You worked a regular W-2 job and had no involvement in his business. The IRS comes after you for $25,000 in taxes and penalties years after your divorce. Innocent spouse relief could eliminate your entire liability.

Who qualifies:

- Spouses who genuinely didn’t know about unreported income or improper deductions

- People whose ex-spouse created tax debt without their knowledge

- Situations where paying would cause economic hardship

Who doesn’t qualify:

- Spouses who knew about or participated in the understatement

- People who significantly benefited from the unreported income

- Situations involving typical marital financial decisions

Application process:

- File Form 8857 within specific timeframes

- Provide detailed documentation about your knowledge and involvement

- Be prepared for IRS investigation into your role

8. Insolvency Exclusion: Relief When Debt Forgiveness Creates Tax Problems

Here’s a situation most people don’t see coming: when creditors forgive debt, that forgiveness usually becomes taxable income. But if you’re insolvent when the debt is forgiven, you might not owe taxes on it.

How debt forgiveness becomes taxable: Let’s say a credit card company forgives $15,000 of your debt. The IRS treats that as $15,000 of income – money you received by not having to pay it back. Normally, you’d owe taxes on that “income.”

If you’re insolvent when debt is forgiven – meaning your debts exceed your assets – you can exclude some or all of the forgiven debt from taxable income.

How to calculate insolvency: Add up all your debts, then subtract the fair market value of all your assets. If debts exceed assets, you’re insolvent by that amount.

Example:

- Total debts: $85,000

- Total assets: $60,000

- Insolvency amount: $25,000

- Credit card forgives $15,000

- You can exclude the full $15,000 from income because you’re insolvent by $25,000

Form 982: You’ll need to file Form 982 to claim the insolvency exclusion. This form requires detailed calculations and supporting documentation.

When it applies:

- Mortgage debt forgiveness during foreclosure

- Credit card debt settlements

- Business debt forgiveness

- Any situation where debt cancellation creates taxable income

Why it matters for tax debt: If you’re already struggling with IRS debt and other creditors start forgiving obligations, insolvency exclusion prevents those “gifts” from creating additional tax problems.

The catch: You must reduce certain tax attributes (like net operating losses or basis in property) by the amount of excluded income. This can create future tax consequences.

Who should consider it:

- People with significant debt forgiveness from multiple creditors

- Those facing foreclosure or business closure

- Anyone whose total debts exceed total assets

This often requires professional help because the calculations can be complex and the tax consequences significant.

The 1099-C Tax Trap: When Debt Forgiveness Creates New Tax Problems

Here’s what nobody tells you about debt forgiveness until it’s too late: when a creditor cancels your debt, the IRS often treats it as taxable income.

Get $30,000 in credit card debt forgiven? Congratulations – you might owe taxes on $30,000 of “income” you never actually received.

This is where Form 1099-C comes in, and it’s critical you understand it before pursuing any debt relief.

What triggers a 1099-C

- Any canceled debt of $600 or more

- Debt discharge through settlement negotiations

- Foreclosure with deficiency forgiveness

- Credit card charge-offs after settlement

- Business debt forgiveness

Understanding the form’s key sections

- Box 2 shows the amount of discharged debt – this is what becomes taxable income

- Box 3 includes any interest if it was forgiven along with the principal

- Box 6 contains an identifiable event code explaining why the debt was canceled

When canceled debt ISN’T taxable

You can exclude canceled debt from income if you qualify for these exceptions:

- Debt discharged in bankruptcy (must meet bankruptcy requirements)

- Insolvency at the time of discharge (your debts exceeded assets)

- Qualified farm debt or real property business debt

- Qualified student loan forgiveness programs

- PPP loan forgiveness (specific to pandemic relief)

The insolvency calculation that can save you

If your total debts exceeded your total assets when the debt was forgiven, you can exclude that forgiven amount from taxable income up to the amount you were insolvent. You’ll need Form 982 to claim this exclusion.

Critical warning: Even if you don’t receive a 1099-C, you’re still legally required to report canceled debt as income. The IRS gets copies of these forms directly from creditors – they know about your forgiven debt whether you report it or not.

This is why settling debts outside of qualified programs can backfire. You solve one problem (the original debt) only to create another (tax debt to the IRS). And unlike the original creditor, the IRS has extraordinary collection powers.

Professional Help vs. DIY: The Honest Cost-Benefit Analysis

Some tax resolution work you can handle yourself. Other situations require professional expertise.

DIY makes sense for:

- Simple penalty abatement requests

- Basic installment agreements under $50,000

- Currently Not Collectible applications with straightforward hardship

Professional help is worth it for:

- Offer in Compromise applications (complex calculations required)

- Multiple tax years or entity types

- Collection statute expiration date analysis

- Cases involving business taxes or payroll issues

- Situations where you’ve already tried DIY and failed

How to find legitimate help:

- Look for enrolled agents, CPAs, or tax attorneys

- Avoid companies that guarantee outcomes

- Get fee agreements in writing

- Check Better Business Bureau ratings and state licensing

The IRS Debt Forgiveness Scam Industry (And How It's Robbing You Blind)

Now it’s time to kill the biggest myths – the ones making scammers rich and taxpayers broker.

Myth #1: “The IRS has a secret debt forgiveness program”

Wrong. Every legitimate tax resolution program is published in the Internal Revenue Code or IRS regulations. If it were secret, how would these companies know about it?

Myth #2: “Settle your tax debt for pennies on the dollar”

This comes from Offer in Compromise marketing, and it’s mostly bull. The IRS accepts offers based on your ability to pay, not your desire to pay less. If you can afford $50,000 but only offer $5,000, you’re getting rejected – period.

Myth #3: “The IRS has a one-time forgiveness program for everyone”

Nope. There are specific programs with specific qualification requirements. Some people qualify, most don’t.

Myth #4: “Call now – this program expires soon!”

IRS programs don’t have expiration dates like grocery store coupons. They’re based on federal law and IRS policy. The only deadline you need to worry about is how long the IRS has to collect from you.

How to spot the scammers:

- They guarantee results before reviewing your case

- They demand large upfront fees

- They claim to have “inside connections” at the IRS

- They use high-pressure tactics or “limited time” offers

- They promise to eliminate debt without knowing your financial situation

What legitimate tax professionals actually say: “Let’s review your financial situation and see what options might apply to your case.” That’s reality-based advice.

State Tax Debt: A Different Animal Entirely

If you owe both federal and state taxes, here’s something that’ll shock you: state tax agencies are often way more aggressive than the IRS. And that’s saying something.

The IRS gives you 10 years to collect, then they’re done. Many states? They’ll chase you forever. Literally no time limit.

The IRS has to follow federal procedures and give you notice before seizing assets. States can move lightning fast with less warning.

Your options get much worse at the state level too. In Texas, the absence of a state income tax simplifies the equation to federal debt only, but Travis County property liens add pressure fast. Our Austin IRS debt relief attorneys handle both federal debt resolution and county lien disputes for clients across the metro.

The IRS has multiple programs – Offers in Compromise, hardship status, payment plans. Most states? Pay up or we’ll make your life miserable.

California files liens quickly and rarely settles.

New York will shut down your business licenses and professional credentials – can’t work, can’t pay, they don’t care.

Illinois loves aggressive wage garnishments that can leave you with almost nothing.

Here’s the smart play: handle your federal debt first. The IRS usually has better options and established procedures. Once that’s settled, use it as leverage with your state. Don’t apply to both at the same time – it just complicates everything and weakens your position.

Bottom line: states don’t play as nice as the federal government. And the federal government isn’t exactly known for being nice.

Let’s make the distinction clear:

| Feature | IRS (Federal) | State (Varies) |

|---|---|---|

| Statute of Limitations | 10 years (from assessment) | Often no statute or longer windows |

| Lien Process | Federal lien; requires notice | May file liens faster, with fewer protections |

| Payment Flexibility | Offers in Compromise, hardship options | Varies widely; often less flexible |

| Collection Tactics | Gradual escalation | Sudden garnishments, license suspensions |

| Transparency | CSED can be calculated | Many states don’t publish expiration rules |

Making the Right Decision for Your SItuation

Tax debt doesn’t improve with time. While you’re researching options, interest compounds daily and the IRS’s collection tools become more aggressive.

Start with an honest assessment of your situation:

- How much do you actually owe?

- What are your assets and income?

- Can you afford some form of payment plan?

- Do you qualify for legitimate relief programs?

Don’t get caught up in marketing promises about miracle solutions. Focus on programs that fit your actual circumstances and have realistic chances of success.

At Silver Tax Group, we’ve been handling tax resolution cases since 2008. We’ve seen every type of situation and know what works in the real world, not just on paper. More importantly, we’ll tell you when you don’t need our help – because the best resolution is often the simplest one.

Contact us today for an honest evaluation of your tax debt situation. We’ll explain what options actually exist for your specific circumstances and help you avoid the expensive mistakes that keep people trapped in tax debt for years.

Because when it comes to tax debt, hope without a realistic plan is just procrastination with interest charges. And the IRS doesn’t forgive procrastination.

Common Questions Regarding IRS Debt Forgiveness

Does the IRS have a debt forgiveness program?

The IRS has multiple debt relief programs, but no single “debt forgiveness program.” Legitimate options include Offer in Compromise (settlement for less than owed), Currently Not Collectible status (temporary collection suspension), penalty abatement, and the 10-year statute of limitations. Each has specific qualification requirements and procedures.

Is IRS debt forgiven after 10 years?

Yes, tax debt expires 10 years from the assessment date under the Collection Statute Expiration Date (CSED). However, this period can be extended through various actions like filing bankruptcy, submitting an Offer in Compromise, or leaving the country. The IRS also becomes more aggressive as the deadline approaches.

Who qualifies for IRS debt forgiveness?

Qualification depends on which program you’re pursuing. Offer in Compromise requires proving you cannot pay your reasonable collection potential. Currently Not Collectible status requires demonstrating that payment would prevent meeting basic living expenses. First-time penalty abatement requires three years of prior compliance. Each program has specific financial and compliance criteria.

How much will the IRS usually settle for?

The IRS typically accepts settlements equal to your “reasonable collection potential” – your asset equity plus 12-24 months of disposable income. For example, if you have $10,000 in asset equity and $300 monthly disposable income, expect minimum settlement around $13,600-$17,200. Offers significantly below this amount face automatic rejection.

What is the IRS hardship program?

Currently Not Collectible (CNC) status provides relief when collection would prevent meeting basic living expenses. The IRS suspends collection activities but debt remains, with interest and penalties continuing to accrue slowly. Status requires comprehensive financial disclosure and regular review of your circumstances.

Can I negotiate my tax debt myself?

Simple penalty abatement requests and basic installment agreements can often be handled without professional help. However, Offer in Compromise applications, complex financial situations, or cases involving multiple tax years typically benefit from professional representation due to strict qualification requirements and complex calculations.