When you run your own business, almost everything can seem more complicated. You have to manage your own accounting, write your own paycheck, and figure out how to manage taxes. One important thing you need to know about as a business owner is filing quarterly taxes.

The IRS requires that all self-employed people pay estimated taxes each quarter. Not only is this the law, but it can also help make your tax burden easier at the end of the year. Read on to learn more about how filing quarterly taxes work.

What Are Quarterly Taxes?

As the name suggests, quarterly taxes are filed each quarter instead of at the end of the year. This may sound like a heinous chore – after all, who wants to pay taxes more often – but it can make your Aprils much more pleasant. Not to mention if you run a small business, the IRS requires you to file quarterly taxes.

Quarterly taxes aren’t a full tax filing like you do in April, and you’ll still need to file your annual tax return each spring. Instead, these taxes are estimates based on your tax return from the previous year. You pay the amount you estimate you’ll owe for each quarter and then settle up with the government during your April filing.

Why File Quarterly Taxes

The most important reason to file quarterly taxes is that the IRS requires all small business owners to do so. We’ll talk more about the requirements for those who have to file quarterly in a minute. But failing to file quarterly taxes if you meet those requirements can get you in trouble during an audit.

The other major reason to file quarterly taxes is that it makes your tax burden easier in April. If you’re making $50,000 a year and are paying a 15 percent tax rate, you’ll be paying $7,500 in taxes each year. Those payments will be much easier to manage in $2,000 installments than in one big chunk every spring.

Who Should Be Filing Quarterly Taxes

The IRS requires that if you make more than $400 in untaxed income each year, you must file taxes on that income. And if your tax requirement is more than $1,000 a year, you must file quarterly taxes. If your business is a corporation and you’ll owe more than $500 in taxes for the year, you must also file quarterly.

But the truth is even if you don’t meet the strict IRS requirements, it’s still a good idea to file quarterly taxes if you make untaxed income. If you’re making less than $15,000 a year from your own work, a $1,000 bill is going to hit you hard. It’s smarter to spread that cost out through the year.

Look at Last Year’s Tax Returns

The first step to filing quarterly taxes is to take a look at your tax return from the previous year. This is going to be your basis for how much you pay on your estimated taxes. Take a look at the total amount you paid in taxes last year and divide it by four; the result will be your estimated tax amount.

If you don’t have a tax return for this business from the previous year, take a look at your best month so far and multiply that by twelve to get your estimated annual income. Take a look at what your tax percentage was last year and use that to determine your total tax responsibility. Then pay a quarter of that every three months for your estimated taxes.

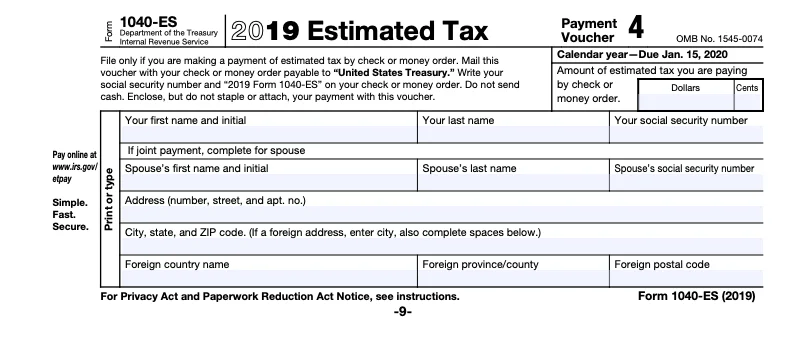

Fill Out a Form 1040 ES

Once you’ve calculated how much you need to pay in estimated taxes, it’s time to pay the piper. You’ll need to fill out a Form 1040 ES each quarter when you submit your estimated payment. This will clarify what your income is and what your tax responsibilities are. This is also where you can remedy miscalculations.

If your business is doing better than you expected, you can correct your estimated taxes when you fill out your Form 1040 ES. If you aren’t doing well as you’d hoped, you have a couple of options. You can request a refund, but we’d recommend you apply the surplus to the next quarter’s taxes.

When to Pay

There are four required dates by which you must file your quarterly taxes. The first of these is the same tax day as everyone else: April 18 of the year in which you earned the income. So you’ll pay taxes on the money you earn in January, February, and March 2020 in April 2020.

The following tax dates are spread three months apart. Second-quarter taxes for income from April and May are due June 15, and third-quarter taxes for income from June, July, and August are due September 15. The taxes for September through December are due January 17 of the following year.

How to Submit Payments

Paying your estimated tax each quarter is a simple process thanks to the ease of online tax filing. In the past, you had to print off your Form 1040 ES and mail it to the IRS with a check. And if you prefer, you can still handle your quarterly taxes this way.

But most people prefer to pay through the IRS Payments Gateway. You’ll have the option of paying with a credit card, making a wire transfer, or pulling the money directly from your bank account. You can also set up a payment plan for your taxes or delay payment if you need to.

What Happens If You Miscalculate or Miss Quarterly Taxes

It may seem like your quarterly tax payments are just a convenience to keep you from paying huge amounts at the end of the year, so why should it matter if you miss a payment? But skipping an estimated tax payment can have serious consequences. You may find yourself facing penalties if you miss the quarterly tax payment deadlines or fail to pay enough on your taxes each quarter.

For every month your payment is late, the IRS may penalize you 5 percent of the amount due, up to 25 percent of the total bill. If you leave your bills unpaid for more than two months, the IRS will tack on an additional $100 fine. If your bill is for less than $100, they’ll double the amount you owe.

Do They Need to Be Equal Payments?

It may seem like you have to pay your taxes in four equal payments. But for people like lawn care companies or chimney cleaning services, you may earn most of your income in a few months out of the year. Paying more during certain quarters can help make less flush quarters easier.

You can split your quarterly tax payments however you like as long as you’re paying some amount in each quarter. If you don’t calculate your first payment until after April, you can roll that payment in with your June payment (though you will have to pay the late fees). And if your business picks up in June, arrange to pay 50 percent of your tax bill on the September payment and divide the other 50 percent among the other three payment periods.

Taxes to Consider

There are a number of taxable sources you may need to take into consideration when you’re estimating your quarterly taxes. The most obvious of these is your self-employment taxes, which are your net earnings from your self-employment. But if you’re able to work your deductions and exclusions in such a way that you don’t have to pay regular self-employment taxes, you may still have to pay an alternative minimum tax.

If your wages are more than $200,000, you may have to pay some additional Medicare taxes and net investment income taxes. If you have a household employee such as a nanny or cook, you may also have to pay FICA and FUTA taxes on their wages. If you have any questions, it’s a good idea to talk to a tax expert.

About Safe Harbors

The trouble with estimated taxes is that, well, they’re estimated. You can’t be sure that you’re paying the right amount, and the IRS can penalize you if you pay too little on your taxes each quarter. But safe harbor taxes protect you from those penalties if you’re within $1,000 of the amount you needed to pay.

If this is your first year paying quarterly taxes, the best policy is to pay 100 percent of what you paid last year, divided out into four quarters. Once you get a better handle on how much you’ll owe each year, you can drop that number to 90 percent and pay the other 10 percent in April. The exception to this policy is if you expect to earn less in the next year than you did in the last.

Adjust as You Go

Even if you do start paying your taxes in four even installments, you aren’t locked into that number for all four quarters. It’s best to stay flexible. Your income might change through the course of the year, and the best policy is to adjust your tax payments as you go along.

Each quarter, look at what you made during those months and pay out the appropriate amount. If you made more than you expected, go ahead and pay in the increased amount. At the end of the year, if you overpaid, the IRS will send you a return on those taxes.

Get the Deductions

When you’re figuring up your estimated tax, don’t forget to take out your deductions. These are any expenses that are related to your business. If you have a home office, this can include a portion of your mortgage, your electric bill, your internet, and any other business-related expenses.

Add up all eligible deductions for a quarter and subtract that number from your total income before you figure out the tax you owe. So if you earn $50,000 and you have $10,000 in deductibles each year, you’ll use $40,000 as your taxable income. That means you only pay $6,000 in taxes instead of $7,500.

Keep Up with Tax Laws

If you’re going to pay estimated taxes each quarter, it’s a good idea to keep up with the current tax laws in your state and on the federal level. These can change from year to year, and 2020 and 2021 are likely to see some major tax shifts thanks to the election.

Staying up to date on current tax laws will help you better estimate how much you need to be paying in taxes. There’s no sense in paying in 20 percent of your income if your tax bracket is only responsible for 15 percent. But likewise, you don’t want to pay 15 percent all year and then discover that you’re on the hook for the other 5 percent.

State Tax Considerations

In addition to your federal taxes, you’ll need to pay taxes to your state as well. When you’re filing estimated taxes, you don’t need to worry about your state taxes. Your payments to the IRS should cover that amount as long as you’re looking at your total tax payment from last year.

Get Help Filing Your Quarterly Taxes

Filing quarterly taxes may seem like a pain in the rear, but it’s a great way to stay on top of your taxes. And if you’re making more than $15,000 a year in untaxed income, the IRS will require you to pay those quarterly taxes. Set reminders for a few weeks before the taxes are due and stay up to date on those payments; you’ll be glad you did come April.

If you’d like to get help managing your taxes, get in touch with us at Silver Tax Group. We provide everything from audit defense and tax fraud investigations to unfiled tax returns and emergency tax services. Contact us today and make sure your financial situation is secure in the coming year.