You know the drill: the dreaded notice has arrived in the mail, and the IRS is now asking you for money. Whether you owe a few hundred or several thousand dollars, being hassled by the IRS is definitely stressful and a bit confusing.

If you’ve got an official notice that says you owe money, don’t panic. Luckily, there are some things you can do to stay out of trouble and get the IRS off your back.

While it’s usually a wise option to consult a professional CPA or a tax attorney, here are some things you can do to help keep the nation’s largest collection agency at bay.

Go Ahead and Pay

While the total dollar amount you owe seems intimidating, it might be best to pay what you owe and get it over with. If you don’t have access to the cash, the IRS offers several payment options.

You can use your credit card, home equity, or even take money from your 401(k) to pay off your IRS debt. Just keep in mind that some options might have a higher interest rate than what the IRS is charging you.

If it’s an affordable amount or one that you think you can repay from other sources, go ahead and stroke a check in full. If it’s not an amount you can handle at once, the IRS does offer several different repayment plans that you can apply for so you can pay it down. These plans allow you to make installments, plus the cost of fees and interest.

Things to Keep in Mind

Just remember that the IRS charges interest as soon as they recognize the money is due, and this can really add up over time. Consider alternative ways to pay it all at once so you can avoid these excess charges.

In order to qualify for an installment plan, all your taxes must be currently filed. For example, you can’t request a repayment plan for back taxes owed from two years ago if you have not filed for the current year.

You can reach the IRS by phone and a representative can help walk you through the process. In most cases, the repayment plan must be approved and there is a one-time fee attached to it once it’s agreed upon.

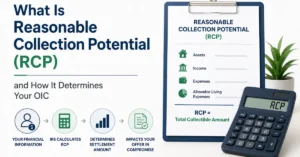

An Offer in Compromise Could Get the IRS Off Your Back

If you see serious financial troubles on the horizon, an offer in compromise might be a better alternative to your tax woes. This program offered by the IRS involves you paying a one-time lump sum that is less than the total amount you owe.

The offer in compromise program is beneficial if you have a lot of cash reserves, but not enough to pay the total amount due. The IRS will review your request and determine if you qualify for this program.

It is very important to note that if you make an offer in compromise payment, this amount is nonrefundable. Even if the IRS denies your request, they’ll keep that money and apply it to whatever you owe.

OIC Tips

While your offer is being evaluated, the IRS will temporarily suspend any collections on your account. Most of the time they expect a lump sum payment of at least twenty percent of what you owe to start with. Next, they’ll decide on a remaining periodic payment until the newly agreed upon amount is paid off.

While this program is fairly risky, it’s often worth a shot if you think it will be approved. The purpose is to show good faith in your intent to repay the IRS while still asking for forgiveness of the total amount.

All told, the offer in compromise plan could save you quite a bit of money in fees and interest in the long run. Make sure you understand the current requirements and guidelines before you go this route just to ensure all of your ducks are in a row.

Fight and File an Appeal

Sometimes, the IRS makes mistakes or you may have forgotten to include pertinent information on your return that has now gotten you in hot water. In cases like this, it could be best to try and file a request for an appeal.

You will need to create a thorough written request and send it to the IRS Office of Appeals. You’ll then be assigned an appeal date, where you’ll need to appear before a representative at your local IRS office.

Some people opt to hire a lawyer to represent them for the appeal, while other people simply provide additional documentation to plead their case. If you feel confident that the IRS is in error, it’s absolutely imperative that you have all of the necessary backup documentation. Write out exactly what it is you think the IRS missed and how you can prove that there is less money owed than what has been stated.

Before your actual appeal, you will need to send something called a formal protest. This formal letter is sent to the IRS and should give them a clearer picture of where you think they went wrong.

Formal Protest Letter Formatting

When you send a letter in protest, you’ll need to state the following:

- All your pertinent information including your name, address, and current telephone number

- A statement showing your intent that you want the notice to be petitioned and sent to the Office of Appeals

- A copy of any documentation or letters you received showing any proposed changes

- Some or all of the tax periods in which your protest applies

- Why you disagree with the IRS (this should be clearly stated for each item you encounter that you feel is incorrect)

- Any and all facts you have to support your claims

- If there a specific law that supports your argument, clearly state or include a copy of the law

- A penalty of perjury statement (you can find the exact wording on the IRS website)

- Your official signature and date

Once you’ve sent the letter, the IRS will review it and notify you of an appeal date, location, and time. Be prepared to speak to a representative from the IRS on your appeal day. Make sure you have everything with you so that you can effectively plead your case.

Tell them to Back Off

Sometimes, it’s just a simple matter of telling the IRS to leave you alone when you’ve run into trouble. While this sounds simple, there’s actually a formal process in place for this, too.

Something called a CNC, or Currently Not Collectible will notify the IRS that you simply cannot repay them due to financial hardship. While this won’t totally absolve you from what you owe, it can help to put their collections process on pause.

In order to qualify for this, you will need to demonstrate that you’re currently coping with financial hardships. The IRS will take a look at all of your “positive income” and compare it to your current net disposable income.

Figuring it all Out

In order to calculate whether or not you’re dealing with financial hardship, the IRS takes your total income and compares it to four main categories based on national standard amounts. These categories include:

- Food, clothing, and miscellaneous expenses

- Out-of-pocket healthcare expenses like prescription medications, copays, and medical supplies

- Housing costs and utilities including a standard scale for rent, property taxes, and basic utilities like gas and electric

- Transportation including things like car payments or costs for public transportation

Keep in mind that the IRS uses a set dollar figure to compute these costs. They will then add them up and deduct the total from your net disposable income. If the final result puts you at an unfair economic advantage, the IRS will typically approve the CNC.

Once your CNC is approved, the IRS will stop all levies and garnishments and will suspend any collective actions. Keep in mind that getting a CNC does not wipe your tax debt clean. Instead, it offers you a temporary reprieve from the stress and financial strain that IRS collections can bring.

Periodically, the IRS will reevaluate your financial situation. If they find that you’ve had an increase in income or your situation has improved, they’ll restart the collection process.

While CNC can really help those in a financial bind, it’s important to note that you will continue to accrue interest while everything is on hold. You’ll also need to continue filing your annual tax returns as normal. The amount of time a CNC is effective can vary depending on your unique situation.

Try the IRS Fresh Start Program

A good way to keep the IRS off your back and stay out of trouble is to enroll in their Fresh Start Initiative. This program is designed to streamline your payments and keep them as low as possible while you pay off your debt.

Recently, the IRS has added credit card payments to your monthly expenses, thereby lowering the amount you would need to pay each month. These payments are now part of the Allowable Living Expense Standards.

When the IRS looks at your future income, they’ll only look at one year’s worth if you plan to repay everything within a five-month period. If you need to pay what you owe for a period ranging from six to 24 months, the IRS now looks at the two years’ worth of future income.

If you have a tax debt of $50,000 or less, you should be able to qualify for the Fresh Start Program. As long as you can repay everything before a total of six years has passed, the IRS will forgive several added charges. These charges include everything from interest and penalties to wage garnishments and liens on your property.

Get a Fresh Start

If you’re almost certain that the amount you owe the IRS is correct, the fresh start program is probably the best route. It will help you avoid the scary scenarios of threats to take your home and garnish your wages. And, it will alleviate the stress that often comes with owing the government money.

In most cases, the payments should be affordable so you won’t need to sacrifice making payments for other things like living expenses. You can contact the IRS directly about this program or speak to a tax attorney who can help you get set up.

The Fresh Start Program can be initiated at any time and will give you the peace of mind you need to get the IRS off your back. It is also important to note that if you’ve been unemployed for more than 30 days, the IRS should forgive added penalties.

Keep a good record of all your financial information including monthly expenses and paystubs. This can help you in the event that you need to show the IRS solid proof of your income vs your monthly expenditures so you can get the payment amount that will work best for you.

Don’t Panic

When it comes to having trouble with the IRS, it’s important that you stay calm and don’t panic. Explore all of your options and read the documentation that you’ve received with care.

If you think the IRS made a mistake, don’t be afraid to file for an appeal. In many instances, appeals are approved and you end up without a balance.

For others, the Fresh Start Program or asking for a Currently Not Collectible status gives people the time and space they need to get back on track. Take a look at all your options so you can get the IRS off your back.

For more information about finances, tax repayment plans, and legal advice, be sure to visit our website.